April, 17, 2026

By Andrea Pescatori, Krishna Srinivasan

Asia entered 2026 on a strong footing. Despite the region bearing the brunt of US tariffs last April and persistent trade policy uncertainty, growth was resilient in 2025 and trade remained robust. Now, the war in the Middle East and the ensuing energy supply shock are raising inflation, weakening external balances, and narrowing policy options, underscoring the region’s dependence on imported oil and gas.

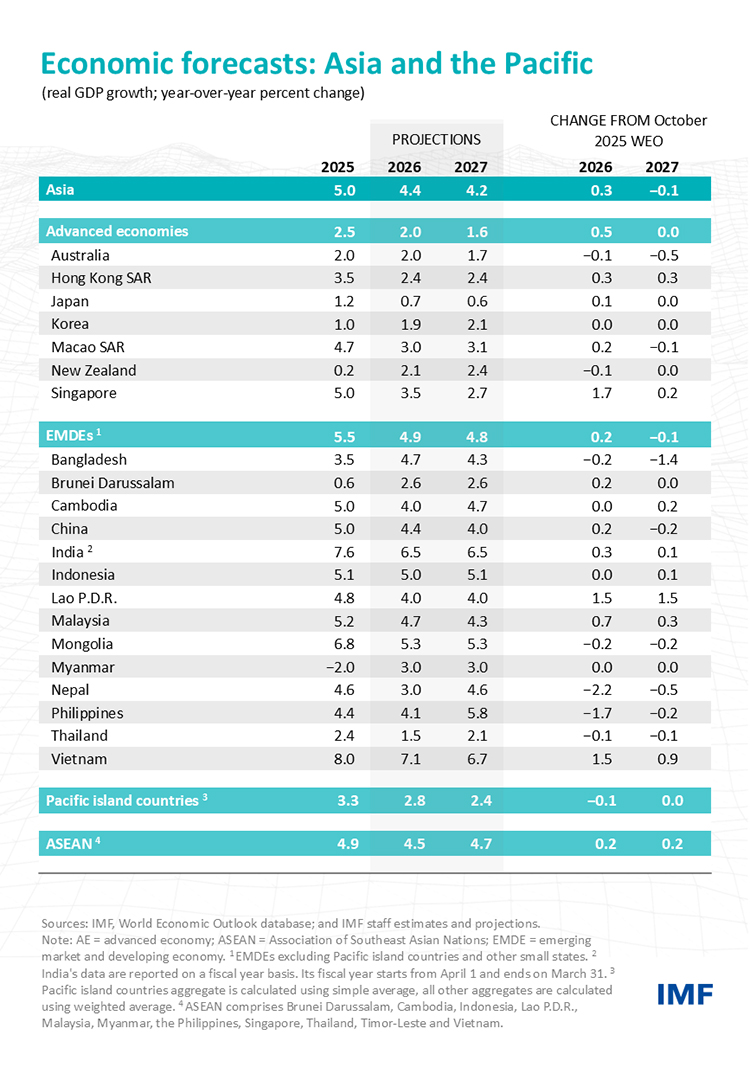

Even so, we project Asia to remain the main driver of global growth. The 5 percent expansion last year will moderate to 4.4 percent and 4.2 percent this year and next, according to the reference forecast in the latest World Economic Outlook that assumes the energy shock proves transient. We expect China and India to contribute 70 percent of the region’s growth.

The headwinds will test Asia’s resilience. Inflation will rise to 2.6 percent this year, 0.4 percentage point more than our January forecast and up from 1.4 percent last year. Should the shock persist or intensify, as in the WEO’s adverse and severe scenarios, growth through 2027 could be reduced cumulatively by 1 to 2 percent.

Resilience amid shock

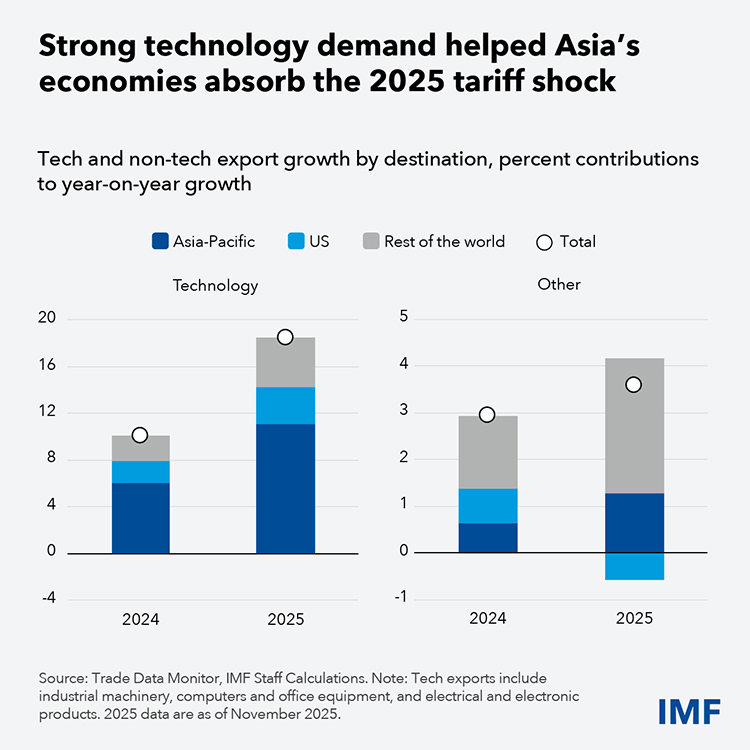

Growth across many economies in Asia was stronger than previously expected in the second half of last year, helped by the robust technology cycle, domestic policy support, and broadly accommodative financial conditions. Demand for semiconductors and related products remained strong, benefiting economies like Korea, Malaysia, and Singapore that are deeply integrated into tech supply chains. Trade within Asia picked up, while diversification toward the rest of the world helped cushion softer demand from the United States, especially for non-tech exports.

Domestic demand, however, remained uneven. Consumption recovered at different speeds across countries, while investment stayed soft amid uncertainty and country-specific shocks.

War tests resilience

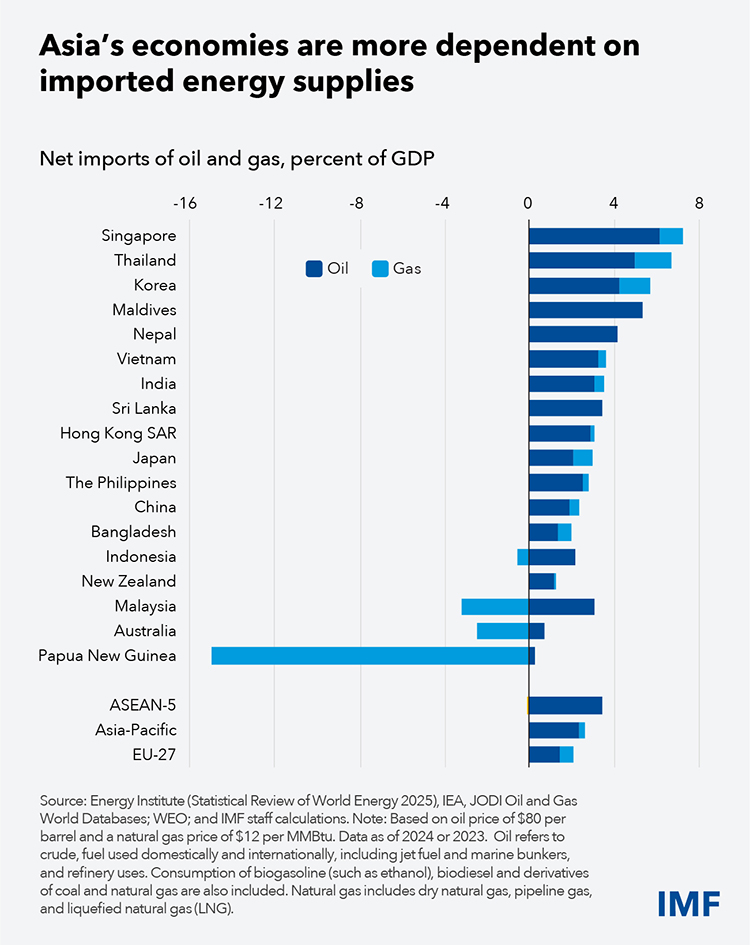

The war introduced a new and more immediate headwind clouding the near-term outlook for Asia, where net oil and gas imports equal about 2.5 percent of economic output.

Asia consumes about 38 percent of the world’s oil and 24 percent of its natural gas. It’s also one of the largest crude refiners, accounting for about 35 percent of global refining capacity, which is heavily concentrated in China, India, Korea, and Singapore.

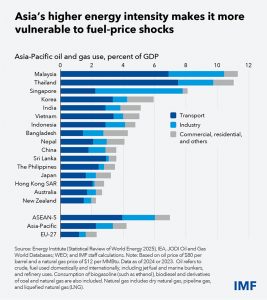

The region’s oil and gas use amounts to about 4 percent of gross domestic product, nearly double Europe’s share. It exceeds 10 percent in economies such as Malaysia and Thailand, where transport and industry play larger roles. These countries and others also rely on gas-fired power plants—and liquefied natural gas imports. Import dependence in many economies reflects limited domestic capacity, manufacturing intensity, and production that relies on oil and gas.

Energy shock

Asia is the main buyer of oil and gas shipped through the Strait of Hormuz, accounting for about 80 percent of LNG exported through the waterway. This is a direct shock to Asian refiners, utilities, and factories. The disruption also may cause local shortages of petroleum products and gas, especially in countries with limited stockpiles. Disrupted deliveries of fertilizers, petrochemicals, and materials like helium and sulfur raise the risk of broader supply-chain disruptions if the conflict persists.

Transmission channels

The effects feed through the broader economy through several channels. First, high energy prices worsen the terms of trade for net oil and gas importers, transferring income to fossil fuel exporters. Second, higher fuel and electricity prices reduce people’s real incomes. Third, because energy is an input into transport, industry, petrochemicals, and fertilizers, the shock raises production costs across the economy, reducing business profits and, over time, feeding into broader second-round inflation pressures. Finally, there is a financial channel. Higher bond yields, a stronger US dollar, currency depreciation, and higher risk premia—notably for fossil fuel importers—magnify the impact of the shock. Within this general picture, country-specific factors, such as fossil fuel intensity of production or petroleum pricing regimes, also matter for the impact.

The shifting outlook

Under the reference forecast, Asia’s growth baseline is broadly unchanged from January, but with higher inflation, weaker external balances, narrower policy space, and larger downside risks.

Across most of the region, growth is projected to moderate. One exception is Korea, which benefits from strong links to the technology cycle. Emerging Asia remains the main global growth engine but is projected to slow by about 0.5 percentage points to 4.9 percent this year, then stabilize next year. A similar deceleration is expected for Advanced Asia. Within the region, growth in Southeast Asia and Pacific island countries is also expected to decelerate, but with considerable variation.

Inflation is also rising. In emerging Asia, inflation is projected to increase from 1.1 percent in 2025 to 2.6 percent in 2026, driven in part by upward revisions in China and India. In advanced Asia, the pickup is more mixed: inflation pressures have eased in Japan, but remain persistent in Australia, where the 2026 inflation forecast has been revised up significantly.

Heightened risks

The reference forecast assumes a conflict of limited scope, with disruptions fading gradually over the year. However, a longer or larger energy supply shock, broader trade disruptions, or renewed policy uncertainty would materially weaken growth, raise inflation further, and tighten financial conditions. Policy buffers would erode and room for additional support would narrow.

Under the WEO’s adverse scenario—where the energy supply shock is larger and fading more gradually compared to the reference scenario—GDP growth in the major economies of the region would decline by almost 1 percentage point in 2026 relative to the reference scenario, with larger losses in more import-dependent and fossil fuel-intensive economies.

In the severe scenario—where the energy supply shock is even larger and lasting well into 2027 before fading——the adverse growth impact would naturally be even larger, with growth in the major economies with a cumulative output loss of about 2 percentage point by 2027 relative to the reference scenario. Headline inflation would be 2.3 percentage points higher in 2027. The impact would again be larger in more energy-exposed economies in the region.

In general, this would disproportionately hurt economies that rely on imported energy, have limited fiscal space, or are highly exposed to the Middle East conflict through remittances, tourism, or commodities such as fertilizers. This is especially relevant in parts of South and Southeast Asia, and Pacific island countries. Sri Lanka, for example, depends on imported oil as well as remittances and tourism transiting from the Gulf. In some agriculture-dependent economies—Lao P.D.R., Nepal, and Myanmar—higher fertilizer costs could lower incomes and raise food prices.

Policy responses and priorities

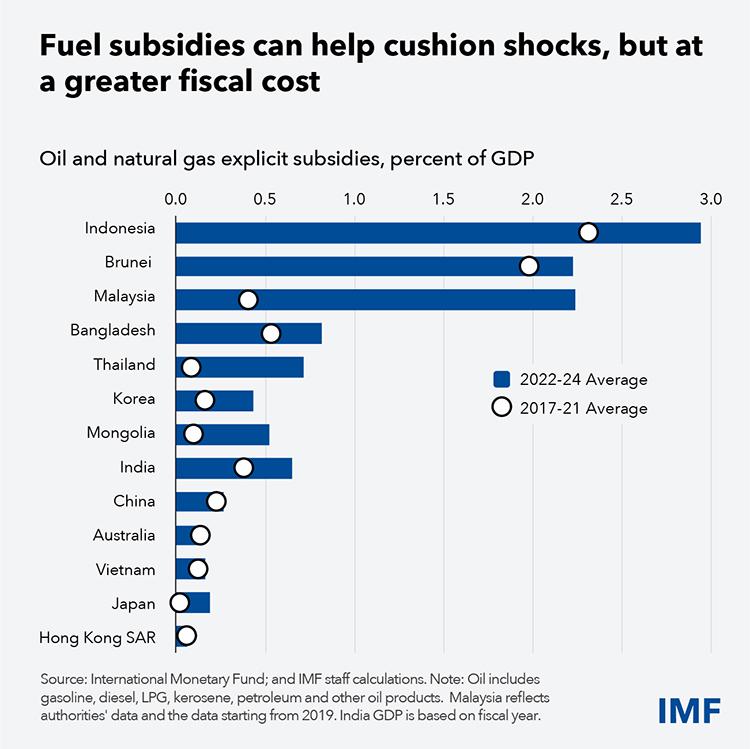

Asia’s governments are taking various steps to address prices and consumption, including encouraging working from home. Several have used subsidies, fuel funds, tax changes, or retail price controls to limit the effects on people and businesses. These measures can be popular in an emergency and help contain temporary dislocations. But muting the important signals that people get from prices won’t lessen the shock. Rather, they may forestall reducing demand.

For central banks, inflation expectations remain broadly anchored so far in most economies. That gives some room to look through the first-round rise in headline inflation. But monetary policy should remain agile. A prolonged energy shock could weaken currencies and generate more persistent inflation.

Interest rates in advanced economies are generally expected to remain on hold or tighten to maintain disinflation. In Japan, where inflation expectations are rising to near target, the central bank can look through the first round of the energy shock and continue withdrawing accommodation. By contrast, where inflation is already above target and domestic demand pressures remain firm, such as Australia, the scope to look through the shock is more limited. In economies where inflation remains below target, such as Thailand and the Philippines, further rate cuts can be paused to preserve room for easing later

Exchange-rate flexibility should remain the first defense. Intervention should be limited to addressing disorderly markets, consistent with the IMF’s Integrated Policy Framework.

Fiscal support should be temporary and targeted at vulnerable people and viable businesses. Cash transfers can supplement personal income. Support should be financed by reprioritizing budgets. This is important in a region with less fiscal space since the pandemic and rising interest burdens. If not feasible, authorities should clearly communicate consolidation plans. Broad fuel subsidies, tax cuts, and general price caps may smooth inflation in the short run, but they are costly, often regressive, and hard to unwind. In fact, higher energy prices can quickly raise fiscal costs, not only by triggering new support measures but also by making existing fuel subsidies more expensive, as in 2022.

Room for support varies. Sri Lanka and Cambodia can provide support, but it should be targeted and consistent with rebuilding or preserving fiscal space. More constrained countries, such as Bangladesh, face sharper tradeoffs because limited room in budgets reduces scope for broad support.

Finally, the shock strengthens the case for structural reforms. Stronger social safety nets would help protect people without general subsidies. Policies to balance job-rich growth and stronger domestic demand would reduce dependence on external demand. In many Asian economies, youth unemployment is still high, and skill mismatches limit productivity and inclusion. Artificial intelligence could widen these gaps if adoption remains uneven—or expand opportunity if accompanied by the right policies on skills, inclusion, and governance. More integrated regional trade, services, and investment would strengthen resilience. And investment in energy efficiency, power grids, and alternative energy would help protect against future fuel-import shocks.

Video Story