July, 1, 2026

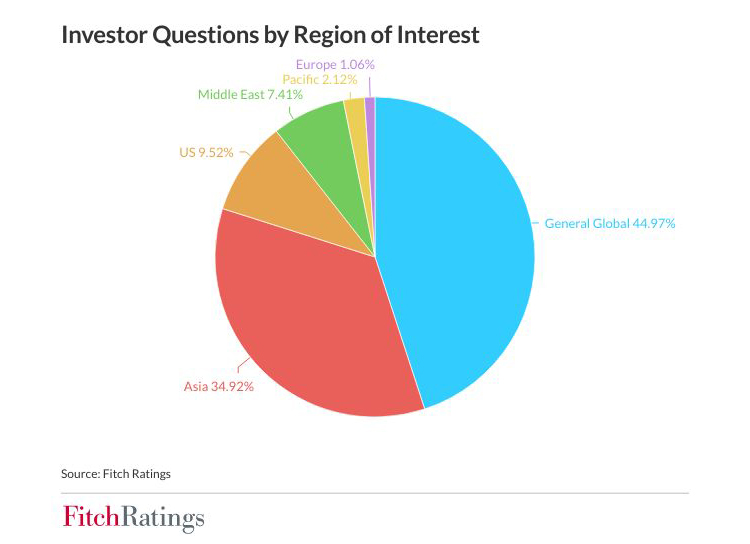

Fitch Ratings: Institutional investor engagement across Asia in June 2026 reveals a strong focus on structural and increasingly embedded risks, Fitch Ratings says. Artificial intelligence (AI) disruption, private credit expansion and sovereign risk have dominated conversations among leading investment teams and official-sector participants in Hong Kong, Seoul, Singapore and Tokyo.

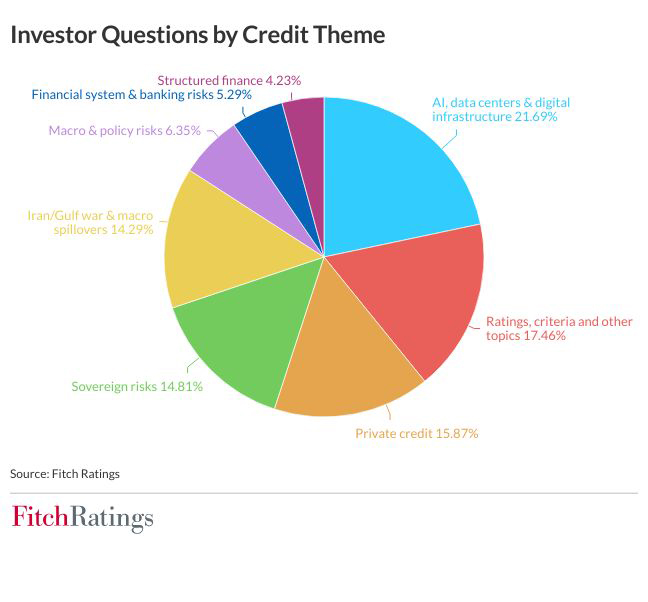

AI and digital infrastructure overspend are emerging as key drivers of global credit risk. Investors are closely monitoring completion risk, high capex and pricing pressure alongside potential equity-market correction spilling into credit as hyperscaler contracts remain highly bespoke and capital availability tightens. We believe AI will drive efficiency gains, but flag risks from labour displacement and eroding tax bases, especially in developed markets.

While private credit is unlikely to pose a systemic threat in isolation, investors highlight intensifying asset competition and opacity risks stemming from the use of layered fund finance structures, such as net asset value loans, obscuring leverage and creditor positioning. Returns are also declining as capital chases yield. Our data show higher default rates in direct lending than in collateralised loan obligations, but recovery rates remain high, as many defaults – classified under our criteria – are resolved by sponsor, borrower and lender collaboration. Portfolio transparency and manager selection are critical for managing these risks, yet Asia-based investors face limited disclosure on US middle-market borrowers. Greater retail and retirement-account participation could raise liquidity and valuation risks, particularly if slower asset exits delay cash returns and managers rely on fresh inflows for liquidity.

Investors are demanding robust oversight in private credit, with attention on rating criteria and market practices. Fitch’s private letter ratings incorporate the same analytical standards, criteria and committee processes as public ratings, but the market remains concerned about the consistency of standards applied by newer rating agencies.

Indonesia (BBB/Negative) enters this period with stronger buffers than in past crises, but investors are weighing these against policy credibility, inflation, currency volatility and ad-hoc funding measures. Investors also question the role of Danantara – the country’s new sovereign wealth fund - and its implications for fiscal transparency and contingent liabilities, alongside how evolving commodity-export policies and more centralised decision-making will shape capital flows and governance. We see regional contagion risk as well below 1997 Asian financial crisis levels, supported by improved transparency, a stronger banking system, higher foreign-exchange reserves and greater policy flexibility across Asia. However, downside risks could rise if currency pressure intensifies, policy credibility weakens or investor confidence or governance erodes in Indonesia, with fiscal and external metrics the key rating triggers.

We view Japan (A/Stable) as one of Asia’s more resilient credits, although investors point to longer-term pressure on the fiscal position, ageing demographics, rising debt-servicing costs and the risk of monetary policy falling behind the curve. We also believe Korea (AA-/Stable) remains resilient, with energy dependence and won weakness offset by strong technology performance. The greater medium-term risk is concentration in a small number of tech issuers, which could amplify equity and external volatility if the cycle turns.

Macro volatility, driven by Gulf tensions and supply-chain disruption, persists. After the prospective peace deal, investor focus has shifted from immediate systemic shocks to residual and indirect effects. We assess the direct credit impact so far as modest. However, downside risk could re-emerge if the peace deal is not implemented and tensions re-escalate, keeping uncertainty high.

Video Story