January, 16, 2025

Small and Medium-sized Enterprises (SMEs) sector has been identified as the most crucial sector of strategic importance to re-orient the country’s economy considering the sectorial contribution to the economy which is more than 50% to the country’s Gross Domestic Production. Nevertheless, the recent upheavals experienced by the country during last few years, following the 2019 Easter Sunday Attack, the COVID-19 pandemic, 2022 economic collapse and other external impacts, have severely affected the SMEs, hindering their capacity significantly, grappling to conduct business as usual. This affected their prompt repayment behavior and led to take legal actions by banks and threat of confiscation their securities/assets by the banks due to default. For the period of 01.04.2019 to 30.09.2024, approximately 494,000 loans amounting to Rs. 886 Bn have been classified as stage 3 loans (Non-performing Loan – NPL) in the banking industry. It is noted that 99% of number of loans categorized under stage 3 are below Rs. 25 Mn. Considering all the factors, a relief package was designed by the government to support the SMEs who faced difficulties in servicing their debt due to the adverse impact experienced during the recent past.

The relief package was developed in collaboration with the Central Bank of Sri Lanka (CBSL), the Sri Lanka Banks’ Association (Guarantee) Ltd. (SLBA), SME sector representatives, applicable government agencies and the relevant measures have been prepared with a long term insight to provide a breathing space for the affected SMEs while ensuring the stability of the banking sector.

The SMEs which meet the below mentioned criteria are eligible to enter the proposed relief package.

A. Specific reliefs

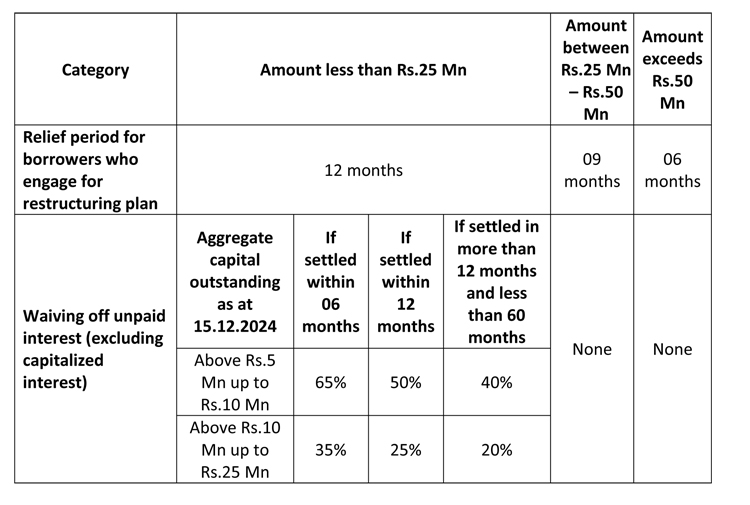

1. Specific relief measures have been proposed under three categories based on the aggregate capital outstanding of credit facilities available as of 15.12.2024 and each category is entitled to specific benefits which are shown in the Table below.

B. General reliefs

C. Additional relief measures

In addition to the aforesaid specific and general relief measures, the Ministry of Finance, Planning and Economic Development has requested the CBSL to explore the possibility to incorporate the following additional relief measures to the relief package in order to ensure the smooth implementation and the maximum benefit to the SME sector.

D. Additional policy measures to assist SME sector

1. Establish an Advisory Committee for SMEs under the leadership of Ministry of Industries as a prime arm for SME policy development, to provide guidance and coordinate all the relevant stakeholders’ work under different institutions for SME sector developments, gathering under one umbrella.

2. Introducing a scorecard/rating mechanism in collaboration with the Institute of Chartered Accountants of Sri Lanka and other professional accountant bodies to support SMEs to increase their ability to access finance.

3. Providing backup support by offering credit guarantees for bank loans of SMEs alleviating collateral issues in obtaining bank loans in collaboration with the National Credit Guarantee Institution Limited (NCGIL) which is to be commenced its operation from January 2025.

Video Story