March, 18, 2026

A prolonged Middle East conflict could create new credit challenges for developed market (DM) sovereigns in Europe and Asia, primarily through higher energy and borrowing costs, rising inflation and weaker economic growth, Fitch Ratings says. Fiscal support measures to cushion households and firms could weigh on budget deficit and government debt trajectories, while financing conditions could become less favourable if risk sentiment deteriorates. Sovereigns with higher debt and structural deficits, and those facing worse inflation-growth trade-offs, are more vulnerable to a sustained shock.

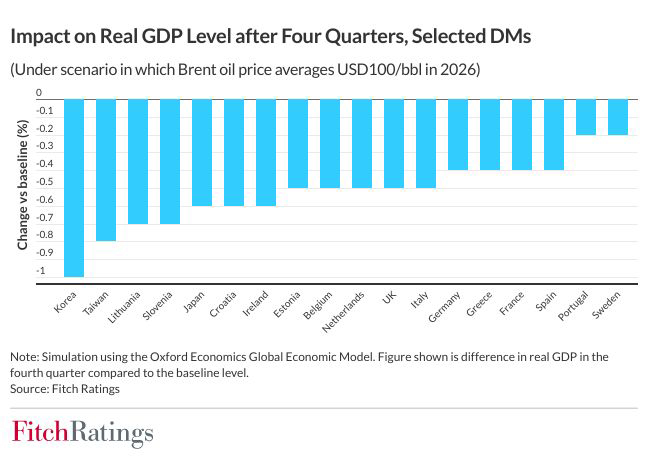

Higher-than-expected oil and gas prices, feeding into higher inflation, would be the most direct channel of contagion, with spillover effects for real incomes and domestic demand. Our baseline is that Brent oil prices remain close to current levels through March, before easing to average USD70 a barrel (bbl) for 2026. A simulation using the Oxford Economics Global Economic Model suggests that an alternative scenario of oil at USD95-USD100/bbl for the whole of 2026 would slow growth across DMs, potentially bringing some countries close to recession.

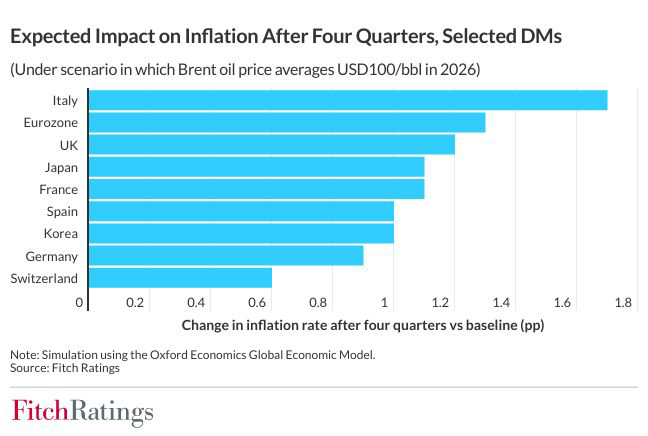

Our simulation suggests that inflation risks are most acute in Italy, the UK, Japan and France among the large DMs, given their energy supply composition. The adverse economic growth impact is greatest for Korea, Japan, the UK and Italy, reflecting a larger hit to household consumption as higher energy and transport costs erode real incomes.

Among smaller DMs, the growth impact varies more widely, with the greatest effects in parts of central and eastern Europe, including the Baltic states and Slovenia, as well as Taiwan. In western Europe, Norway is the only country that is insulated, reflecting its energy-exporter position and stronger terms of trade under higher hydrocarbon prices.

External financing and foreign-currency debt channels are typically less important for DMs than for emerging markets. Instead, net fossil-fuel import dependence, the structure of energy consumption, and reliance on gas imports or gas-linked pricing mechanisms will be key, shaping inflation-growth trade-offs and the distribution of pressure across sovereigns.

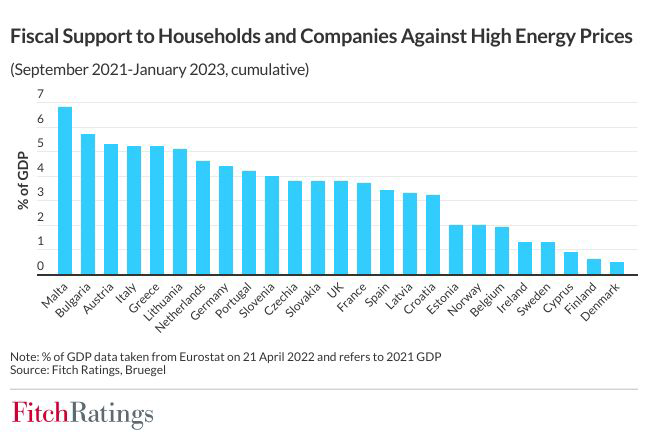

Fiscal policy will respond to higher energy costs in some DMs, even under our baseline. Measures will differ, but could include oil price caps, tax rebates and direct support to households and energy-intensive sectors. In the event of a prolonged shock, the European Commission could ease fiscal rules to accommodate higher spending in the EU via a general escape clause, and we would not rule out an EU-level scheme aimed at reducing financing pressures and supporting policy coordination.

The fiscal cost of such interventions can be material and would add to budget deficits at a time when government debt ratios and financing costs for many DM sovereigns have risen from a few years ago. Weaker fiscal starting positions mean that we would expect any fiscal support measures to be more narrowly targeted than during the 2022-2023 energy price spike, even under our alternative scenario of higher oil prices.

Eurozone government bond yields spreads have risen by an average of 29bp since 27 February. If the higher cost of borrowing is sustained it would add to medium-term fiscal pressures through higher interest costs as debt matures and is refinanced at market yields. We do not view these dynamics as creating near-term “fiscal cliffs” for DMs, but they could reduce room for manoeuvre if the energy price shock persists and growth weakens.

Monetary policy responses will depend on the balance between higher inflation and weaker activity. Under our alternative higher oil price scenario, central banks’ willingness to raise interest rates to curb energy-led inflation effects would be constrained by the weaker demand and employment outlook. Consequently, rate paths may not differ dramatically from the current baseline.

Video Story