The renaissance of so-called State Contingent Debt Instruments, which lure investors with new bonds that promise payouts if the country hits certain economic or fiscal targets, has helped countries from Ukraine to Sri Lanka resolve difficult debt negotiations.

These differ from the bulk of sovereign bonds, labelled "plain vanilla," which pay a predetermined amount in interest over their lifetime before a final repayment.

But SCDIs can be a double-edged sword. Investors are increasingly at odds with the International Monetary Fund's economic projections, said Sergei Strigo, co-head of emerging markets fixed income at Europe's largest asset manager Amundi.

"The only way for investors to get some recovery is through these contingent instruments, but it's not necessarily the best way to proceed in my view, because it's very complicated," Strigo said.

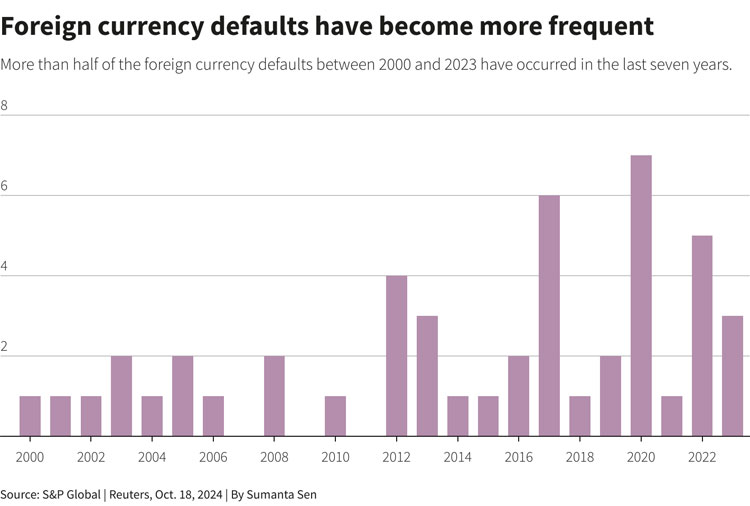

Still, speeding up restructurings is crucial; Zambia took nearly

four years to complete its rework, and Sri Lanka is

still finalising an agreement with bondholders more than two years after defaulting. Whilst in default, the countries lose access to capital markets and funds for investments, from infrastructure to education.

BRIDGING THE GAP

SCDIs are not new; Latin American countries first used them in Brady bonds in the late 1980s after the region's debt crisis. Argentina issued GDP-linked warrants in 2005,

Greece used them as part of its 2012 restructuring and Ukraine added them to its 2015 rework.

History paints a mixed picture on their success.

Researchers at the Bank for International Settlements examining Argentina, Greece and Ukraine in a 2022 report found governments faced a "high and persistent" premium. The mark up demanded by investors, over and above the liquidity and default premium that affected issuers' other bonds, was between 4.24%-12.5% on contingent instruments in the five years following issuance, BIS found.

COURTS AND LACK OF CAPS

Design flaws have also plagued past SCDI instruments.

Hedge funds allegations that Buenos Aires manipulated data and payment calculations ensnared Argentina into

lengthy legal battles over its 2005 GDP warrants, while cash-strapped Ukraine faces billions of dollars in payments for

GDP warrants that did not cap investor payouts.

The troubles helped shape newer instruments.

Zambia's 2024 bond, linked to its debt carrying capacity - an assessment of how much debt a country can carry before the burden becomes too much - as well exports and fiscal revenues, will depend on IMF readings, rather than government statistics.

Experts say those designing new instruments also focus on making sure they are eligible for benchmarks, such as JPMorgan's widely followed Emerging Market Bond Index (EMBI). This is key to keeping investors interested in buying the instruments – and thus government debt costs down.

Ukraine's GDP warrants, for example, were not index eligible, but its August-launched bonds are.

Still, SCDIs come at "a price" for borrowers, said Stefan Weiler, head of CEEMEA debt at JPMorgan, one of the banks on Ukraine debt sales.

"It does create for governments a level of uncertainty that is not really helpful," Weiler said, adding Kyiv had little choice, given the enormous uncertainty surrounding its restructuring.

"Sophisticated investors probably like it, because the chances of (markets) mispricing of the product are higher - there is an opportunity to make a return," he said.

Sri Lanka, which has yet to formally execute its rework, could be a test case. Its recently announced deal would include macro-linked bonds that connect debt repayments with how well it is hitting IMF growth targets, adjusting both principal and coupon payments to the upside and the downside and offering more breathing space in times of distress.

But the country's recent stronger-than-expected growth forecasts have raised questions around how payments will shape up.

Lazard's Cailleteau is optimistic.

"If we succeed that will probably set a standard in terms of intellectual approach to the issue," he said.