Trade and Investment Issues faced by our membership and probable solutions proposed by them.

First of all we would like to thank the government for introducing a package of concessions by circular no 5 of Central Bank of Sri Lanka (dated 25 th of May 2021)

Federation of Chambers of Commerce and Industry Sri Lanka (FCCISL )is the apex body of the Sri Lankan chamber movement giving the leadership to 64 business chambers and associations across the country representing over 25,000 business entities starting from micro level up to extra-large category of business enterprises in the fields of manufacturing, Services, Agriculture and Trading.

We would like to submit key findings of the operational and policy issues faced by our members / Sri Lankan entrepreneurs together with their solutions for your kind attention.

(1)General Business Environment;

There has been a sharp decline of cash flow specially at the retail sectors such as grocery businesses , fish , vegetable, fruits due to less purchasing power of the working class , loss of employment ,and sharp rise in commodities, Most of the SME are unable to cover even current liabilities with their present income. Enterprises are compelled to work with minimum work force therefore there is a risk of increasing unemployment ratio in the country. Enterprises are unable to get any banking facility due to lack of co lateral either their assets have been already mortgaged to the banks or they do not have assets to offer for mortgage.

FCCISL also wish to request the government to seriously consider restructuring loss making State Owned Enterprises such as Ceylon Petroleum Corporation, Ceylon Electricity Board, Sri Lankan Airlines, Sri Lanka Railways, Sri Lanka transport board with a view to reduce the burden on treasury and financiers such as banks and non-banking institutions. Suitable Reforms and productivity improvement in these loss making State Owned Enterprises will help to channel scarce resources for more intensive healthcare measures and modernizing education the much needed basis for future value creation and competitiveness in the economy.

Encouraging investments also featured below as the country moves towards a recovery and comments by respondents included encouraging Foreign Direct Investment, which will help strengthen the balance of payments. This is a good time for the country to attract investment from global multinationals looking to diversify their manufacturing bases; as well as to kick start large scale infrastructure projects that are on hold, by mobilizing private capital.

FCCISL also envisage that some form of wage support for the affected sectors until they regain their normal activity levels, would also be appropriate in order to avoid job cuts and heavy pay cuts. We have identified many common issues faced by industries and have listed out in the following manner.

( a) Issue – Most of the ( SME ) Sri Lankan enterprises are highly illiquid due to loss of sales and the delay in revival is likely to increase the unemployment in the country.

Solution – We request

(1)The government to suspend COVID19 affected business loans for 3 years allowing businesses to recover and start paying at a concessionary rate of interest.

(2)The government to give a presidential decree to all banks to stop auctioning properties mortgaged by customers.

(3)The government to suspend the Parate Execution powers granted to Banks.

(4)To exclude the special clause in the letter of settlement agreement empowering the financial institution to enter and auction in case of failure to settle the facility by financier.

(5) The government to suspend past VAT and Income Tax for 3 years to give a breathing space to businesses.

(6)The government to expedite the establishment of credit guarantee scheme and seriously and consider providing free capital to selected enterprises directly connecting to main economic stream. E g food, agriculture, construction, Exporters, IT ,etc

(b) issue – Even though the new normal advise workers to work from home/remote the legal frame work is not clear as to the workers compensation. There were instances when employers paid 50 % of the wages to their staff members during the pandemic ministry of labor gave a direction to pay the full payment.

Solution – (1)To take in to consideration the emerging work patterns in the new normal and to introduce a proper legal frame by way of a legislation to facilitate work from home/remote work, part time work, contract employment and flexible hours.

(2) Its also recommended to do benchmarking against best practices elsewhere, Sri Lanka too could become more competitive, cost effective and responsive to challenges by having more flexible and modern labour laws.

(3) We request the government to do a national survey / scenario planning about the unemployment of human capital and the skills of this unemployment segment especially due to COVID19.This information is key to make use of very same skills in the transformation of economy to new normal.

(4)Develop a reskilling strategy for the workforce in the sectors where demand will be suppressed for the next 12-18 months. FCCISL is ready to call for a national consultation process with the support of the government.

(2)Issues of Food Industry –

(a)Importation of low quality / substandard fertilizers to Sri Lanka, lack of knowledge on the part of farmers to apply correct quantities,(Irrespective of the type of fertilizer, organic or inorganic,)Lack of knowledge regarding correct application method and correct time to full fill the nutrient requirement of the plant leading to health issues of the consumer.

Solution – we suggest introducing national standards for use of fertilizer having consulted the experts in the field.

(b)Effects of Sudden discontinuation of synthetic agro-chemicals: This would result in a significant yield reduction, affecting farmers’ income and their livelihood, and reducing agriculture-based export earnings. Even though government has categorically stated that Yield loss can be compensated impact of Climate change can offset this relief granted to farmers.

Solution -The government needs to identify an effective mechanism to evaluate and measure such losses, and an efficient system to pay compensation for the affected growers avoiding injustice that may occur in the process.

(C )Issues arising out of Green Socio-economic Model’ approach: FCCISL is fully aware of the need of such a concept and we welcome it .However any loss of food crop production to the levels less than the consumption requirement, especially the main staple rice, will lead to food imports until expected level of establishment of the ‘Green Socio-economic Model’ approach. , if the imported food items do not comply with the acceptable standards under the ‘Green Socio-economic Model’.

Solution - in such instances, any food items imported should be screened to assure compliance to food safety standards and the government needs to improve the infrastructure needed for such screening exercise.

( d) Generic issues arising out of introduction and adoption of new technology; FCCISL fully support this move however its suitability and the impact on Eco system might be an issue

Solution – we need to identify the best practices used in the world related to ecological approaches in agriculture .The suitability in safeguarding our environment should be assessed through simple but well-designed experiments as a top priority, prior to their introduction and adoption. This is true for both imported and locally developed technologies.

(e)Sensitive issues related to introduction of any technology or input such as new bio-fertilizer (imported or locally developed) in a haphazard manner: In case of introduction of new bio-fertilizer (imported or locally developed) to a specific crop situation hurriedly the impact to our agro-ecosystems / microbes -living organisms will have to be assessed since they behave differently even within the same country but in different ecosystems. There is a possibility such a move would destroy our microorganisms and not become pathogenic as well. (Such repercussions are the same whether we use organic or chemical inputs)

Solution – (1) We propose to establish a Research and Development unit under department of agriculture to carry out sensitive studies such as impact on agro-ecosystems / microbes -living organisms.

(f)Lack of Sufficient infrastructure facilities (including accredited laboratories), trained manpower (including scientists, technicians, farmers, and other stakeholders to establish a strong monitoring and evaluation mechanism.

Solutions ; FCCISL request the government to

(1) set up a national Training authority with due Accreditation to bridge the knowledge gap for the future and to set up the strong monitoring and evaluation mechanism.

(2) include Green Socio-economic Model to school curriculum preferably for the G.C.E. (O/L )

( g)Issues related to Wastage of Food from the farm to end consumer; Sri Lanka has a very high wastage of food items –somewhere around 50% due to lack of sufficient cold storage and improvised transportation system.

Solution – (1)Even though there are constructive steps taken in the recent past to construct cold storages the governments are yet to solve this problem satisfactorily. FCCISL suggest to the government to expand the cold storage facilities using solar energy and to grant a special tax benefits for investors.

(2)FCCISL also suggests the government to develop traditional and natural preservatives, which effectively reduce the wastage of food items.

(3) FCCISL encourages innovations to support supply chain and distribution stability, which featured as a high priority, points towards greater opportunities in technology usage by businesses and the state, e.g. strengthening agricultural value chains.

(h)Lack of organic substitute to replace chemical pesticides: Apart from lack of availability of required quantity of organic fertilizer, the industry will also face an issue of as to how to replace the chemical pesticides by organic pesticides or non-chemical based pesticides or traditional methods.

Solution – This is a question without a short-term solution. FCCISL request the government to set up a research and development unit in collaboration with concerned universities to develop effective new technology and systems to answer this question and to conduct awareness programs for farming community. The ancient methods used in Sri Lanka such as using Sera leaves and Cinnamon leaves to protect rice from insects too need to be properly assessed. Sri Lanka also need to learn from best practices related to organic agriculture in the world.

(i) Lack of real time on line data related to Agriculture industry; this affects the industry negatively in many ways (E g the efficiency and effectiveness of distribution of fertilizer (organic or chemical), the effect of climate change and adverse weather conditions on the crop and effective distribution of food (vegetables and fruits) for consumption.

Solution – FCCISL requests the government to set up a technologically advanced real time on line data collection system for the purpose of presentation and monitoring of the industry. This will be a major productivity improvement step. This may also address the issue of delays and alleged corruption related to distribution of fertilizer.

( j)Issue : Lack of technology for fruit and vegetable extraction technology for commercial purpose, ill equipped laboratory system to certify food standards or help innovation and new product development.

Solution – we request the government to seriously consider to improve the capacity of our laboratories so that the proper advises can be given to innovators and new product developers.

Summery – FCCISL understands the government efforts to strengthen the livelihood of the farming community, which is the need of the hour. We have seen fruitful results in increasing production with the government initiatives to ban imports and produce what we can produce in Sri Lanka. Turmeric and mung bean are excellent examples. However, we sincerely hope that the government will strike a balance in having benefits to both farmers and consumers. We recommend this strongly as declining yields by immediate shifting from conventional systems to organic systems is a reality. Therefore, there is a likely chance that many food products would not be accessible due to less availability and less affordable due to higher prices, to a larger community in Sri Lanka. Therefore, we propose a systematic transition as the only option to achieve the overall objectives of this effort.

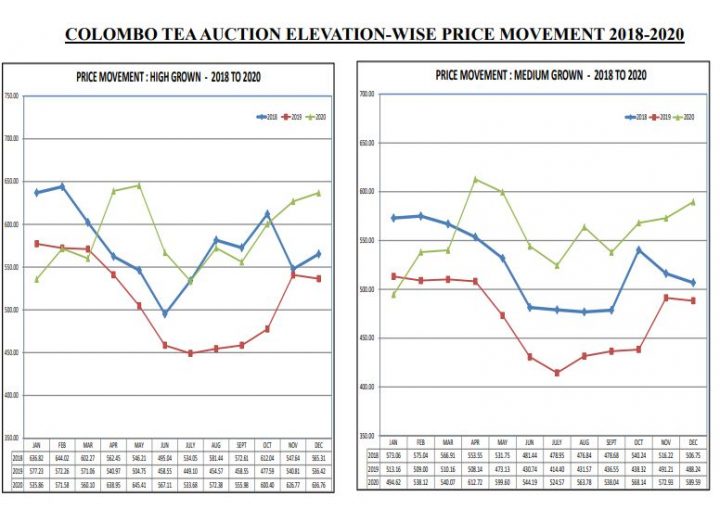

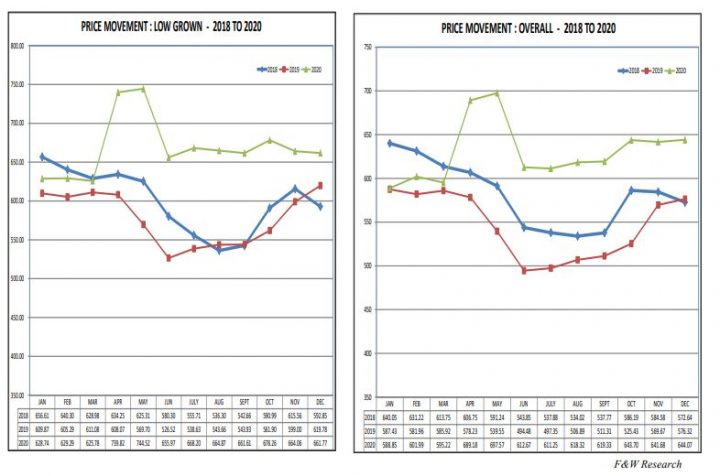

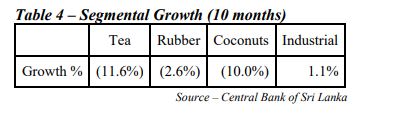

(3)Tea Industry;

Issues- According to expert opinions the introduction of organic fertilizer to Tea Industry may affect the Sri Lanka’s Tea industry in many ways.

E g –(a) .Drastic reduction of average annual tea production of 300 Mn Kg by 50 % ,Inability to product quality black tea. both due to use of organic fertilizer which can not provide minerals such as Nitrogen, posperous, potassium and magnesium sufficiently and according to the life cycle of the tea plant and frequency of tea plucking ( 7-10 ) days.

(b)Less leaves per plant would force tea estate workers to pluck less quantities compelling them to disqualify to their incentives. ( the minimum quantity to be plucked for incentives is around 22- kg-25 kg )If organic fertilizer is used even plucking tea leaves up to 15kg -18 kg will be a challenge.

Solutions – (1) To replace irregular and excessive use of out dated chemical fertilizer by using quality and more ecofriendly chemical fertilizer of 3 rd generation now used in many countries.

(2)To gradually reduce the use of low quality chemical fertilizers and start granting a subsidiary to GAP (Good Agriculture Practices) at agriculture lands.

(3) Initially at the introductory level to have a mix of fertilizer (50 % chemical and 50% organic)

(4)To introduce new soil preservation systems during the transition period.

(5) To introduce organic fertilizer in the following order

( Rice , Vegetable /Fruit and then Tea, Rubber and Coconut )

(4) Construction Industry;

(a)Issues over use of a common and standard letter of contract for all types of contracts with un supportive clauses to solve real issues faced by contractors. . E G No contract form to cater for SME sector, No contract forms for Lump Sum, No provision for Cost Reimbursement. The very same letter of contract is used for Management Contracts, Construction Management, Turn Key projects. Etc.

Solutions – Recommended to revisit the letter of contracts and to introduce project specific letter of contract to Sri Lankan construction industry.

(b) Lack of flexibility in the contract to accommodate Changes in construction Cost.

A sizeable amount of contracts were entered into between the parties (the Contractor and any state agency as the Employer) without operative provision for price fluctuations or in the form of Fixed Price Contracts. Since we are operating in a volatile business environment where drastic price changes are a reality some times due to exchange rate fluctuations the absence of such a provision permitting the contractors to redress the undesirable financial effects of escalation of cost of construction. . It is also noted that in some instances, certain items subject to high cost escalations are not covered in the CIDA formula qualifying for price adjustment.

Solution -.To include provisions in the Standard letter of contract to accommodate price increase of raw materials or any other ingredients above a particular percentage in consultation with the Industry experts.

( c ) Addressing of issues due to consequences of outbreak of COVID - 19 pandemic and Travel restrictions.

Naturally, project delays occurred due to lockdowns and other impacts associated with COVID-19 thereby prolonging and protracting the material procurement schedules. Because of extension of procurement schedules and delay caused to ordering and purchasing lead to price escalations and finally to on time delivery of the project back to owners. Further All contracts, without exception, contain a Liquidated Damages provision. In the absence of Extension of Time, this entitles the Employer to recover such liquidated sums from the contractor in the event the contractor fails to complete the Works by the Time for Completion stated in the contract. In this connection, we notice that the granting of formal extension of time has become a time consuming process predominantly by reason of complex contractual and technical process and internal approval processes of the government. In this context the contractors are genuinely not entitled to Extension of Time grants and thereby exposed to Liquidate Damages in full or in part depending upon the liability for the delay.

Solution – FCCISL requests the government to include a provision in the letter of agreement to waive off Liquidated Damages.Government need to issue a presidential decree to all government agencies not to claim bank guarantees leaving room for private sector constructors and banks to negotiate for an Extension to bonds and guarantees and not to charge liquidated damages.

( 5) Issues in the Rubber industry -

(a)Permission to allow importation of rubber for BOI registered companies from foreign countries due to higher production cost of Sri Lankan rubber industry. This move affects the local rubber prices.

Solution : (1) If B.O.I industries are allowed to import raw material FCCISL propose to impose a levy to match the difference between global and local prices.When the Local market price is higher government can wave off cess charge

(2)An introduction of Real time on line data for monitoring local and international prices ,production ,climate changes ,productivity , world industrial demand for rubber

( b) Issues over environment protection;

Solution - To fix rubber waste water plants to existing treatment plants or to fix same in every industrial zones.

( c)I Lack of growth of rubber trees : In sri lanka there is no substantial interest to grow up rubber trees to replace the the old trees being uprooted annually.

Solutions –To grant subsidiaries for the industry to grow up new treas.

(D ) Lack of Tappers :the demand for rubber is growing but finding enough labor is an acute issue. Reluctance of the younger generation to join the industry have caused added issues to the labour issue

Solution – (1)Rubber research Institute ( R.R.I ) can recruit tappers and provide a training course and then to get them a practical training sessions at J.E.D.B and other plantations. That will encourage the school leavers to learn through awareness programmes to tap even on rainy days and how to use rain guards to protect the milk.

(2)Its also important to make small and medium rubber growers aware of latest trends related to rubber prices.

( e ) low Productivity – Sri Lanka’s productivity related to rubber industry in comparison to Thailand and Vietnam is rather low and finally affect the competitiveness in the world market.

Solutions- FCCISL recommend to form a tappers force , recognition for workers, and Improved quality of life for workers such as introduction of digital technology with REAL TIME ON LINE DATA to improve the efficiency and to make the industry attractive for younger generation.

( 6) Fish Industry –

Issues :(a) Complex system to import raw materials by BOI companies.

Solution - BOI Companies with Processing Factories should be given a very simplified system to import raw material for exporting Seafood products.

(b) No rational selection of categories of Fisheries & seafood production and exports needed to the country.

Solution – To allow Industry to decide which categories of Fisheries & seafood production and exports needed for the country; To Identify the geo- social features and the economic situation of the country (Sri Lanka) and allow Industry to decide which categories of Fisheries & seafood production and exports needed in the country and support such industry for aggressive promotion and marketing.

(c) Lack of a national fisheries and seafood strategy

Solution - Formulating a National Fisheries and Seafood Strategy and export plan and a road map is the first and foremost step the government (Ministry of policy Planning, Ministry of Fisheries, BOI and EDB) has to undertake. Digitalization of the industry and sustainable fishing methods must be incorporated in to the national plan.

( d) lack of focus on efficiency and quality affecting the productivity.

Solutions ;

( 1)The bigger boats over 40 to 55 feet to be upgraded to have RSW system (refrigerated sea water). Since the bigger boats are travelling for more days to catch the fish, their catch needs to be stored properly to maintain its quality. The system ensures better quality than conventional icing of fish.

(2)Introduction of Collector vessels (trans-shipment) to sustain the long line Tune fishing:.Sri Lanka has a fleet of 3000 smaller boats designed to travel up to 100 km ‘s . However these vessels travel up to 700 kms to catch fish and then bringing the harvest to the harbor without any freezing facility. This kind of unsafe method does allow only 50% of the harvest to export and nearly 50 % will not be in exportable condition. In this context we need to follow the strategy adopted by other countries.Thats to introduce collector vessels. We request the Sri Lankan government to take a policy decision to implement this concept. If implement 100 % of the fish harvest will be exportable and will give a big push for Tuna exports.

(3)Encouraging the establishment of Aquaculture farms at Industrial level; we request the government to fully support this move and to encourage the private sector investments by granting low cost funding, tax incentive and other facilities such as suitable sea areas for farming. ( In Sri Lanka Aquaculture contribution to Fishery industry is around 1% whereas the rest of the world has gone far beyond 60 %)

( 7) Ornamental fish :

(a) Issues – Sri Lankan Guppies have a big global demand but due to lack of supply we can not meet the expectations of the buyers.

Solution – FCCISL request the government provide financial, technology and training for the industry to grow. Developing more Breeders ( SME) as a cottage industry -knowledge can be given by ( NAQDA )ideal for cooperative farming advanced technology

(b)Issues : Competitors from Singapore, Thailand, and Malaysia can provide fish at a cheaper price.

Solutions – Request the government to improve productivity through new technology, systems etc.

(c )Issues : Competitors from Singapore, Thailand, and Malaysia can provide fish at a cheaper price.

Solutions – Request the government to improve productivity through new technology, systems etc.

(8) Knitting industry:

(a)Issue ; Unfair competition posed to Sri Lankan knitting industry by fabric importers, who only pay Rs 100 per a kg as CESS which was decided a long time ago. This is a big discouraging factor for the local manufacturers.

Solution: (1) We request the government to increase this CESS to 300 rupees per KG or between 1 usd to 1.5usd per KG so that local manufacturers can compete with imported fabrics.

(2) We also request the government to calculate the CESS based on the weight of the Bill of Lading as opposed to invoice value, which can sometimes be manipulated or subsidized by exporting country.

(b)Issue : increase of production cost is limiting factories to expand and fully meet the local demand

Solution : We request the government to provide the following basic needs as an encouragement to expand the local production capacity.

- suitable Land from industrial estates

- Clean water for dyeing charged on usage

- post treatment (discharge water) at cost

- Steam charge on usage

- 3phase power

Points 1 to 3 require a lot of capital investment depending on production capacity.

(c )Issue ; Lack of consistent government policies with regard to importation of fabrics discourage more investment by local manufacturers.

Solution - if the government policies remain consistent for a particular period of time the local manufactures will set up new factories and plants to improve the capacity to cater to the growing demand of the consumers. Srilanka has the knowledge and capability to produce high quality fabrics to suit the expectations of the Sri Lankan consumers.

( 9) FCCISL’s proposals to encourage investments within the country.

( a) Granting tax amnesty for cash and cash equivalents for 1 year with a view to strengthen the cash flow in the business environment.

(b-1) Special tax concessions can be considered to these investors for the investments related to the agriculture/food security, fishery and who are investing to support the National Export Strategy.

( c) The major barriers which prevents more exports from Sri Lanka to the world is high production cost and lack of productivity in many industries.( at present the Sri Lankan energy cost in the region is very high. This affects production cost and also the pricing for exports and export prospects ) In this context as a tactical move it is recommended to grant a subsidies to Sri Lankan exports and export prospects for a period of 2 years followed by a major productivity drive across all major industries to offset inefficiencies of production processes making Sri Lankan products are more competitive in overseas markets. (on successful completion of the productivity drive the export subsidy can be later withdrawn).

(d)To introduce a special loan scheme and grants to promote sectors identified by national export strategy ( e g Tea, Rubber Gem and jewelry, spices, wellness spa , Electrical,electronic, IT related products ,assembling of vehicles and boat and shipbuilding and other important domestic sectors such as Health ,dairy farming, agriculture, fishing ,transport etc .

( e) New Products for Export basket; In view of COVID19 Sri Lanka needs to encourage its exports and related activities on following sectors such as pharma, waste management, packaging, processed food, telecommunication and high tech products which will have a better demand in the world.

( f) In order to support SME’s the banking system Its recommended to introduce a grant scheme at least upto Rs 2.0 Mn without a collateral from those who cannot provide acceptable tangible securities. The total amount of such loan, in order to protect the banking system may have a cap of the total loan outstanding of the bank etc.

( g) In order to improve capital market the dividend income from listed companies should be exempted from income tax for at least 3 years.

(h) To establish loan risk compensation funds and make appropriate compensation to financial institutions for the non-performing loans issued to small and micro businesses.

(i) We encourage government to issue small and micro financial bonds and construction bonds to collect funds needed to finance SME and construction industry.

(j)In view of the new emerging concepts such as Work From Home and social

distancing our labor laws should be revisited and amended in line with global

competitive environment.

( k) To allow bringing foreign skilled workers for selected sectors such as

mechanical, electrical and electronic to work in free trade zones for 1-2 years.

(l) Providing free lands without rent fee for 10 years for cultivation and agro business purpose backed by sound business proposals etc.

( m)To extend the time limit for recovery of businesses sector wise and according to the epidemic situation, and financial institutions to write off the trade and finance losses according to the provisions if the conditions for write-off are met.

( 10) Issues over attracting Foreign Direct investments,

(a)Lack of clear guidelines to investors

Solution – The Total investment portfolio stack of the country ( E g Infrastructure development Projects/ Treasury Bonds /Debt and equity need of Private Sector ) need to be prepared under one unit and same has to be up dated regularly explaining the projects coming under each sector in the country. This should include the brief description of the nature pf project, unique competitive advantage etc .

(b)No clear guidelines on the Risk and Return to Investors

Solution – There need to be a clear analysis on each project on the risk and return trade off to be in line with the appetite of the investor community.

( c) Mode of funding is not clear ;

Solution – This is where the mode of funding need to be explained whether it is equity, debt or hybrid. This exit route for the investor need to be clearly spelled out.

( d) Lack of clarity on the government policy on Risk management.

Solution; The unique risk factors of investing in each project and how to mitigate these risks need to be explained using how favorable the government policies are.( e g consistent tax structure for 5 years )

( e)Non-availability of wide range of financial instruments, which are available in other countries.

Solutions; Sri Lanka need to introduce financial instruments such as FRB ( Floating Rate Bonds ),RUFs ( Revolving Underwriting Facilities),SPNs(Secured Premium Notes with Detachable Warrants ) and NCDs( Non-Convertible Debentures with detachable equity warrants. )

( f ) Further extension of amnesty granted to foreign remittances, and foreigners who invest in Sri Lanka over USD 500,000/ to grant resident visa up to -10 years. We request the government to consider Tax concessions to encourage large scale investments - eg. five year tax holiday for investments with a value of over USD 5 mn. All export oriented businesses to be tax free for a period of 5 years, irrespective of the industry or size. This is a good time for the country to attract investment from global multinationals looking to diversify their manufacturing bases; as well as to kick start large scale infrastructure projects that are on hold, by mobilising private capital.

( g ) land issues : Government to sort out the issues over lack of suitable lands with electricity and water for foreign investors and to upgrade the facilities at existing 14 free zones.

(h ) Efficient approval process; The Government agencies should be serious about granting various approvals in a shortest possible time and improve the efficiency of the authorization bodies. ( To follow the Ease of doing business guide lines )

(11) On the long term FCCISL wish to suggest following measures to support the

sustainability of the new normal economy.

( a)Development and Venture Capital Banks : FCCISL request government of Sri

Lanka to seriously focus on setting up of development and venture capital banks

under public private partnership to support innovation and digital trade facilitation including E commerce to support new normal economy.

(b)Vocational training institute under BOI :To set up a vocational training institute under BOI to produce skilled labor categories to cater to mechanical, electrical and electronic industries.

( c) Rationalization of HS codes ; Sri lanka’ s HS code are very complex by nature so identification of products using H S codes is very difficult. When this situation exists,Sri Lanka is at a disadvantage at trade negotiations and the threat of agreeing to undesirable tariff lines remain high. In this context as a matter of national priority, we have to rationalize the HS codes before negotiating any trade agreement. This measure would also help the country to comply with WTO requirements.

(d) R & D expenditure :when incurred within Sri Lanka in product development

(excluding marketing) should be given triple deduction for income tax computation (This was allowed before 2018)

(e)National Lean Management authority: Recommend to set up a national Lean

management authority with expressive authority under H E president to implement an aggressive productivity improvement plan across the major industries in the public and private sector to provide the leading edge for Export competitiveness of Sri Lankan products.

(f)National Single Window : Recommend to speed up the establishment of the

national single window proposed by EU trade related assistance to lodge information, and documents with a single-entry point to full fill all import, export and transit related regulatory requirements to reduce the inter agency human interaction that would mitigate the COVID9 due to no human contacts and this system would also reduce the transaction cost for exporters /importers.

(g)National Trade Policy (NTP) : we request the government to formulate a progressive National Trade Policy (NTP) based on national interest, transparency, real economic benefits for the purpose of monitoring and reviewing of trade agreements now in place and to give a strategic direction to future trade agreements. NTP is also expected to safeguard the offensive and defensive interest of Sri Lanka.

(h)Training institute for foreign trade: FCCISL suggest setting up of a training institute for foreign trade to study the global and regional trade and investment trends and engage in Economic modelling and scenario planning at trade negotiations.

(i)Appointment of productivity commission: Government needs to appoint capable and experience members who knows about the productivity and the productivity improvement. This unit should be used as the advisory body to improve the micro economic policy of the government.

(j) Recommends to establish SME development authority (something similar to that of urban development authority) under H E president with expressive authority to give a proper strategic direction to develop and nurture SME;s in the country. Then all SME supportive government agencies can be grouped under this authority.

(k)Introduction of National Housing Pricing (NHP) Index: FCCISL recommends to introduce NHP which indicate the health of the market and the price trends nationally and regionally. It would also tell if the market is weighted towards buyers or sellers indicating the benefits for them. A rational NHP will support and reflect in repayment terms, insurance products to hedge lenders risks. Finally, NHP will avoid sharp artificial price escalations by developers. This would also develop rational mortgage market in Sri Lanka.

(l) Raising Capital through private equity for loss making State Owned Enterprises (SOE);FCCISL recommends even 10 % of the enterprise listing at the Colombo Stock Exchange. That would attract international funding agencies and pension funds.

( m) Economic use of sea area: Finally FCCISL looks beyond it horizons and seriously think that Sri Lanka has come to a point of no return where any further compromising cannot be made between the economic development and the environment. Perhaps any further encroachments in to land may endanger the stability of the whole eco system now based on a thin forest cover around 20% in the country. FCCISL in search of post COVID-19 economic order wish to request the government to explore the possibility of extensively using so far commercially untapped vast sea territory in a sustainable manner. We observe the sea economy in terms of future economic potential may exceed the output of land based (65k km2) economy. Sri Lanka has a sea belt (21 km2) and also has an exclusive economy zone at sea not exceeding 200 nautical miles (altogether 510,000 km2) and with a right to go up to 1,200,000 km2). Certainly the way forward for Sri Lanka is a blend of land based development done so far and future sea based economy, both giving great opportunities for global and local businesses.

FCCISL would like to meet you for a discussion over the matters stated above and sincerely request you to grant us an early date / time convenient for you.

Your’s truly

Shirley Jayawardena

President

CC – Hon Mahinda Rajapaksa – Prime Minster of Sri Lanka

Hon Basil Rajapaksa –The Chair of Presidential Task Force on Economic Revival and Poverty

Eradication.

Dr P B Jayasundera - Secretary To the H E president

Prof W D Lakshman Governor of the Central Bank