June, 19, 2025

Fitch Ratings has adjusted its outlooks for the banking sectors in South Korea, Taiwan, Thailand and Vietnam to reflect weaker prospects for banks in 2025 amid exposures related to US trade policies, though the overall banking sector outlook for APAC remains ‘neutral’. We maintain the ‘deteriorating’ outlook on China’s banking sector, reflecting persistent challenges for banks, as government policies weigh on profitability and banks experience asset quality pressure from a weaker economy and property sector.

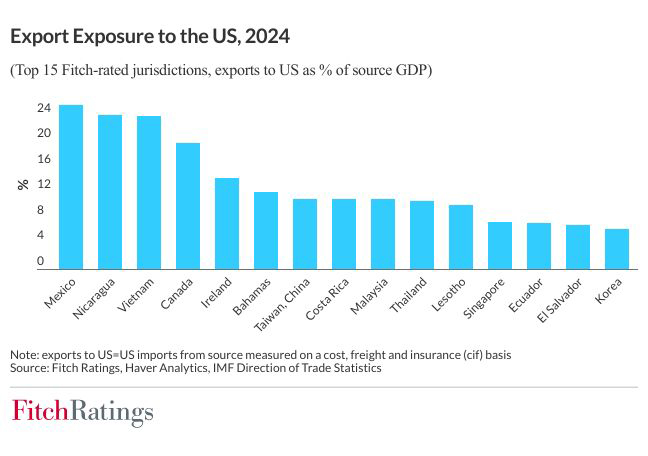

There is great uncertainty around the ultimate trajectory of US tariffs, but APAC’s high degree of trade openness and its exposure to US demand leave it particularly vulnerable to potential US tariff increases. For the most affected banking systems, lower profitability and weaker asset quality will be key channels for contagion from the tariffs. However, the ultimate effects of the trade war on regional bank sectors will depend on final tariff outcomes, their impact on local economic growth, banks’ exposure to vulnerable sectors, and the potential for changes in fiscal, monetary or credit policy.

We have moved the outlook for banking sectors in 2025 to ‘deteriorating’ from ‘neutral’ in South Korea, Taiwan and Thailand, partly because banks’ loan growth, asset quality and profitability will likely weaken in these markets as tariffs rise, given their higher export exposure and sales to the US. Increased uncertainty and volatility associated with tariffs have already diminished near-term GDP growth prospects in Thailand and Korea, particularly amid the soft domestic demand in both countries over 1H25. Policy interest rates could also be lower than we had anticipated in these three markets under a higher tariff scenario, which would weigh on net interest margins (NIM).

Meanwhile, Fitch has moved the banking sector outlook to ‘neutral’ from ‘improving’ in Vietnam to reflect tariff risks. Vietnam has the highest degree of export exposure to the US market of any economy in APAC. We believe that the authorities could persuade banks to reduce lending rates as part of their efforts to support economic activity under a higher tariff scenario, weighing on their NIM. The softer economic outlook is also likely to result in higher credit costs, leading to slower – albeit still solid – profit growth for the year. However, the 2025 system loan growth quota is 16% and could increase further. This, together with possible loan relief and forbearance, may partially offset the pressure on lending yields and provisioning needs, and suggests that non-performing loan rates may rise only moderately.

Tariff risks have reinforced our ‘deteriorating’ banking sector outlooks for China and Hong Kong. The latter outlook also reflects our view that Hong Kong will see the largest rise in non-performing loans in APAC in 2025, due to a lingering property sector malaise. Both systems face subdued loan demand compared to historical averages.

We consider the outlooks for banking sectors in other parts of APAC to be more resilient to higher US tariffs, largely because these economies typically have lower direct export exposure to the US. However, bank asset quality in certain sectors could still be hurt by additional US tariff increases, or by indirect trade effects.

The changes in our APAC banking sector outlooks should have little impact on our banking system operating environment scores, which remain relatively stable. For example, we expect the operating environment for Chinese state banks to remain stable as they maintain steady financial metrics and adequate rating headroom despite near-term tariff risks. Moderate credit growth and risk appetite, along with sustained resolution of non-performing loans in recent years, should help support their financial performance and pressure from tariff escalation is likely to be partly offset by fiscal stimulus.

Video Story