October, 14, 2024

Fitch Ratings: Fitch Ratings believes Asia Pacific (APAC) regional credit conditions could be challenged by trade protectionism, weaker economic growth and mounting geopolitical tensions if Donald Trump wins a second presidential term.

Our analysis focuses on the potential for major policy shifts if the Republican candidate wins November’s US presidential election. We do not assess the positions of his opponent, Vice President Kamala Harris, in detail, but anticipate greater continuity of President Joe Biden’s policy positions if she wins.

Potential US policy changes under a Republican presidency could present several risks to issuers in APAC. Intensified trade tensions may have significant effects for sovereigns and companies that export goods to the US - a risk we highlighted in our recent report on exposures among Chinese corporates.

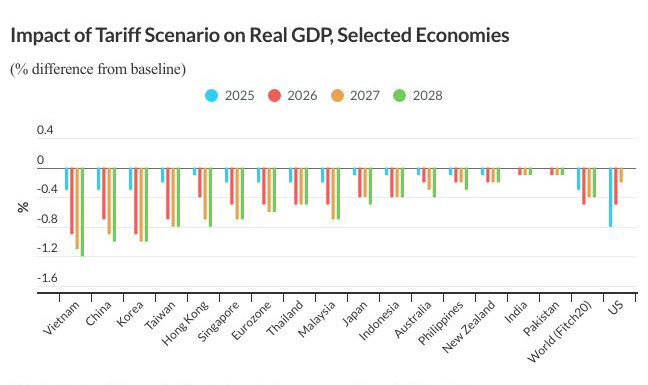

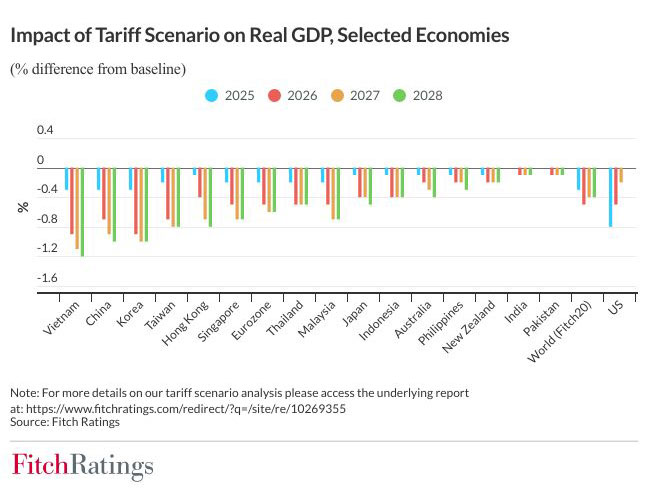

Our scenario analysis further indicates that if US trade protectionism increases sharply it could result in significantly lower growth in several APAC economies. Under a worst-case scenario with retaliation from the US’s trading partners, growth in China, South Korea and Vietnam would be particularly affected, with real GDP in 2028 being 1% or more below the level under our current baseline. India, which is less export-oriented, would be relatively unaffected. Lower interest rates due to a weaker economic backdrop could affect banks' profitability and credit costs, with varying effects across APAC markets.

Geopolitical risks, notably stemming from tensions between China and the US, could be a significant factor for APAC irrespective of the winner of the presidential election, but would be likely to be raised if trade protectionism rises sharply. This could result in a more volatile global economic environment, and potentially put upward pressure on governments’ defence spending, adding to fiscal consolidation challenges.

Video Story