February, 19, 2025

Fitch Ratings-Hong Kong/London-18 February 2025: The US administration’s inclusion of a broad range of factors in its assessment of whether trade relations with foreign trading partners are fair and reciprocal will increase uncertainty over the scale of tariffs that could be introduced, and which markets could be affected, says Fitch Ratings. Sovereigns that have significant export exposure to the US could face additional economic risks relative to our base case, from both the actual introduction of US tariffs and uncertainty over possible tariff outcomes.

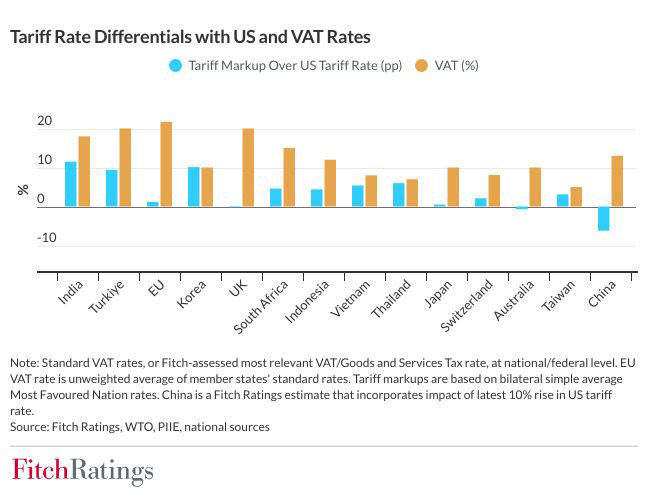

The policy unveiled on 13 February indicates that the US will compare tariff rates charged by trade partners on imports of goods from the US with those currently charged by the US on trade partners’ exports to the US when assessing whether relations with trade partners are non-reciprocal. However, it will also assess a range of other factors, including value-added taxes (VAT), non-tariff barriers such as subsidies and burdensome regulation, exchange rates and wage suppression. The policy directs US officials to propose remedies to the president, based on their findings, in the pursuit of reciprocal relations with each trade partner. Officials have said that assessments could be completed by 1 April, paving the way for follow-up trade actions.

The breadth of the factors being assessed – particularly with the inclusion of VAT – could imply that the US is considering much larger tariff increases than we had previously assumed for some bilateral trade partners. This risk had already been highlighted by the high 25% tariff rates initially announced for most imports from Mexico and Canada, though these were subsequently paused.

Some emerging markets where US exporters currently face high import tariffs and where the trade surplus with the US is sizeable, such as India, could be particularly affected if the US pursues a more reciprocal approach to trade relations. The difference in tariff rates between emerging markets and the US in their bilateral trade tends to be wider than that for developed markets. However, VAT rates are high in many developed markets in Europe, potentially leaving them vulnerable on that vector, alongside a broader worsening of US-EU relations.

The US government’s aggressive trade policy approach may raise additional challenges for trade agreements that face upcoming reviews or expiry. For example, the US-Mexico-Canada Agreement is due for review in 2026, and the preferential trade access to the US market granted under the African Growth and Opportunity Act will expire in September 2025 unless extended.

Fitch’s December 2024 Global Economic Outlook incorporates a US protectionist turn with the US effective tariff rate rising to just under 8% from 2.3% in 2024, but the risk of a much more significant jump in tariff rates is rising. Higher tariffs will weigh on global growth, as noted in our Global Sovereigns Outlook 2025.

We continue to see credit risks beyond our baseline for sovereigns that have significant direct exposure to US demand, linked to the uncertainty around US trade policy, as well as broader, indirect risks for those that have exposure to global demand.

The US government has already shown a willingness to negotiate with individual trade partners, while there is a large degree of uncertainty about how high and how broad the increase in tariff rates will be. However, applying varying tariff rates to different countries would increase the risk of trade diversion, compared with a universal tariff.

Video Story