April, 11, 2025

Fitch Ratings: Sharp US tariff increases will disrupt corporate supply chains and affect economic growth and corporate earnings in APAC and globally, despite the 90-day pause on some of the larger tariff hikes announced on 2 April, says Fitch Ratings. However, few of our rated APAC corporates face a combination of high sector vulnerability, low rating headroom and substantial direct exposure to the US.

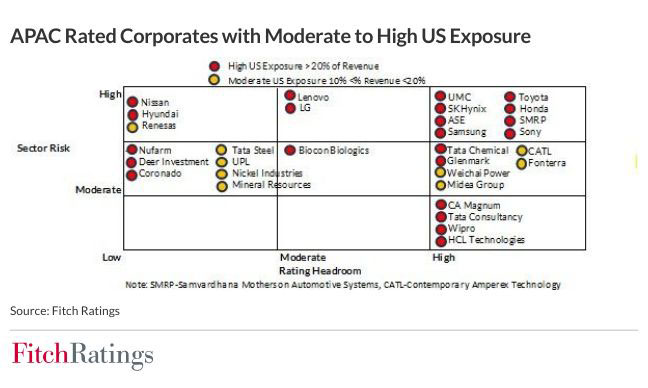

Effective tariff rates on US-China trade have been raised much further than we had anticipated, following retaliatory actions on both sides, and are not yet subject to the 90-day pause. This, coupled with the minimum 10% tariff that remains in place on all APAC exports to the US, as well as various other sector-based tariffs, will hurt APAC companies that sell to the US and Asia’s export-oriented economies. Our rated APAC corporates that have significant US exposure generally have moderate to high rating headroom, offering some buffer to manage tariff uncertainties.

Fitch views the autos, tech hardware, chemicals and metals and mining sectors as most directly exposed to tariff risks as the US adopts a more aggressive approach to trade policy, but few sectors will be left untouched.

Companies in APAC would be vulnerable if the US eventually implements the 2 April tariff hikes in full. Exports from Vietnam, Thailand, Indonesia, Taiwan, India, South Korea, Malaysia and Japan could face much higher US tariffs that would hurt their economic growth and dim corporate earnings prospects. Secondary effects from sharp US tariff increases under such a scenario could pose a threat even to companies with rating headroom, as regional and global growth would likely be significantly lower than we had anticipated.

Video Story