January, 28, 2020

Considering the recent major Fiscal and Monetary policy changes, First Capital Research believes that the current accommodative monetary policy stance is appropriate and that there is ample space for market lending rates to reduce without further adjustment in policy rates. Already announced tax relief, and proposed moratorium on capital repayments of bank loans for the SME sector are likely to provide further impetus to the economy.

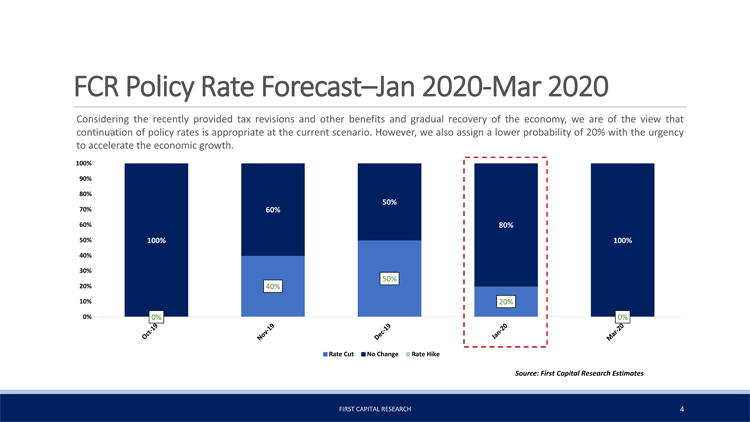

Accordingly, First Capital Research assigns an 80% probability for no change in policy rates in the upcoming policy announcement and expects policy rates to hold in the 1Q2020.

However, First Capital Research assigns a lower probability of 20% for a rate cut in January 2020 with the urgency to boost the revival of economic activities.

“We continue to maintain that SRR is likely to be remained at the current level,” First Capital research added.

Following is the full statement by First Capital:

Previous Pre-Policy report; CBSL maintains its policy rates

In the last policy meeting held in Dec 2019, CBSL maintained its accommodative monetary policy stance at current levels immediately following the tax revisions with the belief that it would support higher economic growth in the short term. Considering the recently provided tax revisions and other benefits, we were of the view that continuation of policy rates were appropriate at that economic juncture. However, we also assigned a 50% probability for a rate cut in Dec 2019 considering the urgency to improve the lending and the economic growth.

Domestic economic activities show signs of recovery

Sri Lanka’s economy grew by 2.7% in the 3Q2019, higher than our expectation of 2.2%, indicating a gradual recovery relative to 2Q2019 growth of 1.6%. Private sector credit growth also recorded an increase of LKR 47.1Bn in Nov 2019, illustrating a positive credit growth for the 4th consecutive month with Jan-Nov 2019 growth at 3.5%, closing in, on our credit growth target of 5% for 2019E. Going forward, a steady revival of economic activity is envisaged, supported by potentially further improved political stability after the General election in 2020 and inline with the measures taken to stimulate the economy such as SME and extended tourism moratorium, tax benefits and Capital Adequacy relaxation on banks.

Extended giveaways!!!

As an extension to the stimulus package previously granted, Govt. took measures to remove DRL imposed on banks and NBFIs and revise downwards the corporate tax rates across all sectors. We expect the additional support given with the above measures to further enhance the growth in the economy. However, government’s ability to bridge the revenue loss due to the recent tax revisions will be a concern leading to a risk in 2020. The stimulus package may potentially lead to fiscal slippage, reducing the possibility of further monetary easing in the near term.

Foreign inflows despite outlook downgrading for SL

Following a similar path to Fitch, S&P recently revised its rating outlook on the Sri Lanka sovereign credit to negative from stable on the view that largerthan-expected fiscal deficit and concerns over indebtedness. Despite the negative rating outlook revision, in line with our expectations, SL’s government securities market witnessed a net inflow since the beginning of the year 2020 amounting to nearly LKR 5.5Bn and is expected to gradually improve during the 1Q2020 with the settling of the political uncertainty to a certain extent.

Inflation to remain at low single digit levels and stabilise within 4-6% while market lending rates are expected to reduce further

Inflation, as measured by CCPI accelerated in December 2019 to 4.8%YoY driven by the food inflation. However, we expect a gradual acceleration in inflation to continue in the first half primarily driven by the supply side shortage relating to food due to the floods in November. However, the inflation is only likely to rise to around 6% mark as tax cuts are expected to partially offset the food inflation. Moreover, market lending rates are expected to continue to adjust downwards in response to monetary and regulatory measures taken by CBSL.

Expectation

Considering the recent major Fiscal and Monetary policy changes, First Capital Research believes that current accommodative monetary policy stance is appropriate, and that there is ample space for market lending rates to reduce without further adjustment in policy rates. Already announced tax relief, and proposed moratorium on capital repayments of bank loans for the SME sector are likely to provide further impetus to the economy. Accordingly, we assign a 80% probability for no change in policy rates in the upcoming policy announcement and expect policy rates to hold in the 1Q2020. However, we assign a lower probability of 20% for a rate cut in Jan 2020 with the urgency to boost the revival of economic activities. We continue to maintain that SRR is likely to be remained at the current level.

Video Story