April, 23, 2026

Fitch Ratings - Emerging markets in Asia would see rising cost pressure across agribusiness and food supply chains if a prolonged US-Iran war pushes fertiliser supply disruption deeper into the planting season, Fitch Ratings says. For these sectors, reduced fertiliser availability and higher prices would raise production costs, discourage application rates and weaken crop yields, which would lead to margin pressure and higher food prices later in 2026.

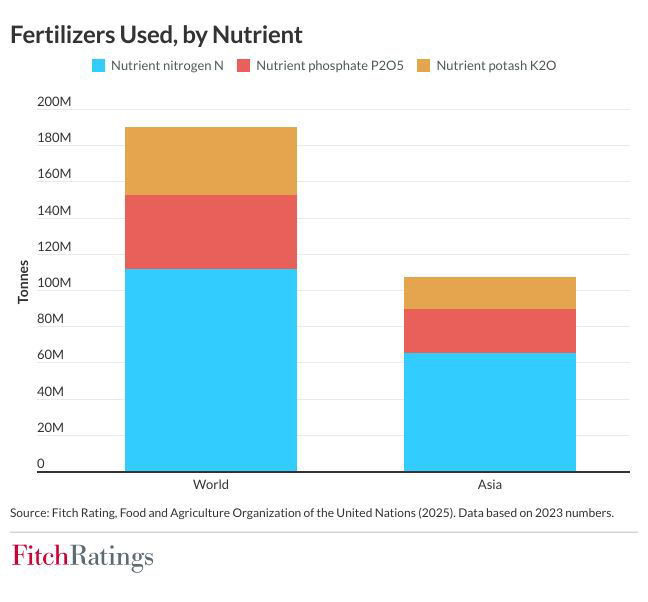

Food cost pressure would rise if fertiliser supply and pricing do not normalise in the near term, especially as some South and Southeast Asian countries enter their sowing season. The Gulf region produces much of the world’s fertiliser as natural gas is an important feedstock. Asia’s supply is exposed if the conflict continues, keeping gas prices high and continuing to disrupt shipping in the region. We also expect key Asian exporters like China to continue restricting fertiliser shipments, at least to the mid-year. This would prolong input-cost pressure for growers and raise the risk of supply disruption for downstream food producers.

Nitrogen-based urea prices have risen by around 50% to around USD700 a tonne from about USD465 before the war. If the high prices persist, farmers may reduce fertiliser use or plant less, increasing the risk of weaker crop yields and higher food prices later in the year.

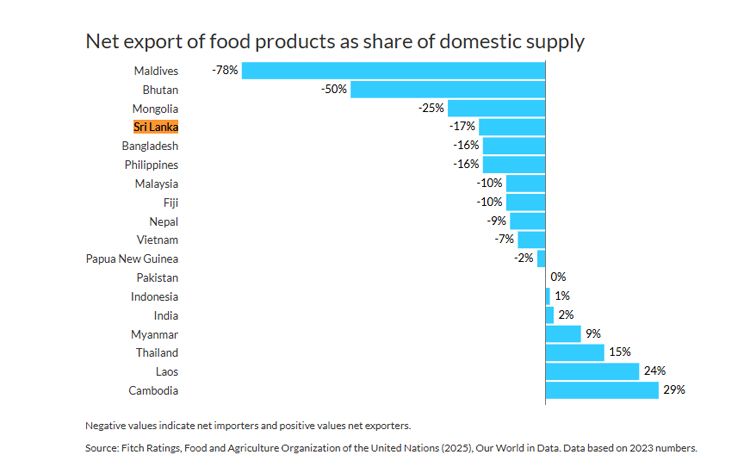

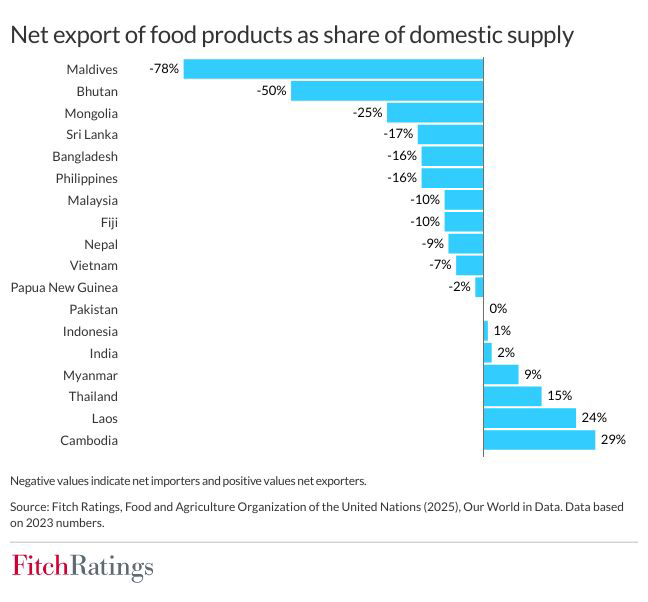

Domestic production remains the main source of food across much of emerging Asia, so reduced fertiliser supply could have a material effect if it weakens planting or yields. Countries that are more reliant on imported food would be more exposed if weaker domestic harvests coincide with elevated global food prices and export restrictions in traditional food suppliers. In net terms, food import dependence is in the mid-teens across the Philippines, Bangladesh and Sri Lanka, increasing to the mid‑20s in Mongolia. In the Maldives this is as much as 78.3%, though this mostly reflects the large, elastic demand from the luxury tourism sector.

Near-term food price pressure remains moderate across most countries where data are available, due to the lagged impact of the energy shock on food prices. However, the World Food Programme estimates that if the Iran conflict does not end by mid-2026 and if oil prices remain above USD100 a barrel, 9.1 million more people in Asia could be pushed into acute food insecurity, 24% more than before the war.

Some countries, like India, have sufficient fertiliser stockpiles for upcoming planting seasons, limiting near-term cost pressure. The shock would pass more directly into farm input prices and, later, consumer food prices in many other emerging Asian markets that have weaker supply buffers.

Crop risks will become more serious if the disruption lasts through the planting cycle and reduces fertiliser application rates. The effect would vary by country depending on crop mix, staple consumption, and the type and intensity of fertiliser use. A Yara International study found crop yields can fall by 43% in a field that goes without nitrogen fertiliser for a year, based on the long-running Broadbalk experiment on wheat growing in the UK. Losses exceed 80% over a longer period. This is not Fitch’s base case, but it illustrates how sustained disruption could alter planting decisions, reduce nutrient use and weaken harvests, keeping food inflation high after the initial oil shock fades.

Fiscal pressure would increase mainly through the corporate and household channels if governments provide subsidies to stabilise fertiliser and food supplies. Where support is limited, higher costs would fall more directly on farmers, food companies and consumers, which could heighten social tensions.

Video Story