July, 3, 2020

Fitch Ratings has affirmed the National Long-Term Ratings of the following four Sri Lankan finance and leasing companies:

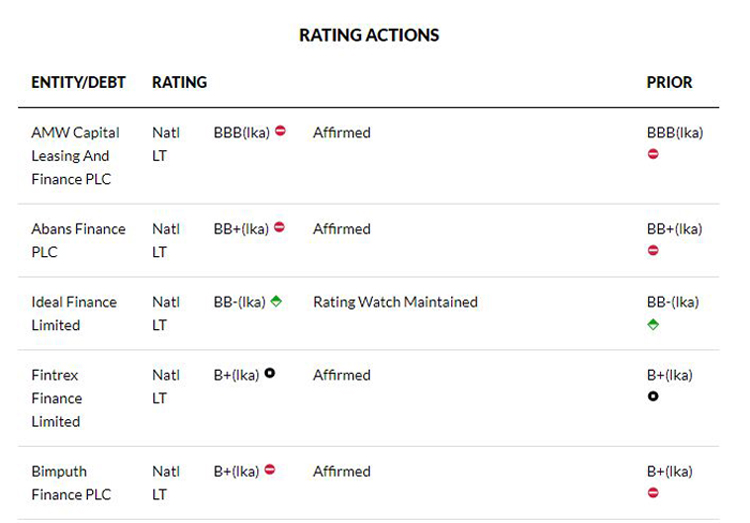

-AMW Capital Leasing And Finance PLC (AMWCL) at 'BBB(lka)'; Outlook Negative

-Abans Finance PLC at 'BB+(lka)'; Outlook Negative

-Fintrex Finance Limited at 'B+(lka)'; Outlook Stable

-Bimputh Finance PLC at 'B+(lka)'; Outlook Negative

In addition, Fitch has maintained the 'BB-(lka)' rating on Ideal Finance Limited on Rating Watch Positive (RWP).

KEY RATING DRIVERS

AMWCL

AMWCL's National Long-Term Rating is driven by Fitch's expectation that its 90% parent, Associated Motorways Private Limited (AMW), will extend extraordinary support, if needed. We believe the finance company is strategically important to its parent, which is a large importer of motor vehicles in Sri Lanka. This is based on AMWCL's role in the group, the common AMW brand and reputational damage to AMW should AMWCL default.

Fitch sees the synergies between the two companies as high because a large share of AMWCL's advances are provided to clients to purchase AMW products. AMW set up AMWCL in 2006 with the objective of supporting its core business.

We see AMWCL's intrinsic credit profile as being weaker than its support-driven rating due to its small franchise and weaker financial profile relative to similarly rated peers.

Abans Finance

Abans Finance's rating reflects Fitch's view that support would be forthcoming from its parent - Abans PLC (BBB+(lka)/Negative) - if needed. Our expectation stems from Abans being the largest shareholder in Abans Finance, the parent's involvement in the subsidiary's strategic decisions through board representation and a common brand name.

Abans Finance is rated three notches below its parent because of its limited contribution to the group's core businesses, in our view. The company financed a negligible share of Abans' consumer durables revenue in the financial year ending March 2020 (FY20). It mainly provides vehicle financing, with nearly a third of its leasing portfolio being to the two-wheeler sales of Abans Auto (Pvt) Limited, a company owned by Abans' shareholders, but positioned outside the Abans group. Abans Finance only contributed 8% of the group's profit before tax in 9MFY20.

Our assessment of Abans Finance's limited importance also incorporates the parent's decreasing shareholding in its subsidiary, which has fallen to 50%, from 89% in FY16, due to capital infusions, mostly via its private-equity investor. In addition, we believe support from the parent could be constrained by Abans Finance's large size, as its assets represented 93% of group equity and 27% of group assets at end-2019.

Abans Finance's intrinsic financial strength is weaker than its support-driven rating due to its small franchise, limited operating history and high-risk appetite. Its reported regulatory gross non-performing loan ratio (NPL) over six months had further deteriorated to 21.6% in FY20, from 18.0% in FY19, to be among the highest in its peer group.

Ideal

Ideal's rating reflects its improved capitalisation following the introduction of new capital by an initial LKR1.1 billion investment in February 2020 from India's Mahindra & Mahindra Financial Services Limited (MMFSL). This has strengthened the company's financial profile and bolstered its loss-absorption buffers against Sri Lanka's challenging operating environment. Ideal's rating also takes into account its high-risk appetite, aggressive growth, exposure to more-vulnerable customer segments and its still-developing franchise, which is reflected in its small market share and limited operating history.

The RWP reflects Fitch's belief that Ideal's rating could benefit from the change in shareholding and increased probability of support once MMFSL's effective control is established, in light of MMFSL's potentially stronger credit profile. As part of this process, MMFSL will progressively invest LKR2 billion (approximately USD11 million) to acquire a 58.2% stake in Ideal in three tranches up to 2021. Fitch expects the minimum regulatory capital requirement of LKR2.5 billion for finance companies to be met at the end of the transaction, at which point we expect MMFSL to have acquired effective control of Ideal.

We believe the challenging operating conditions exacerbated by the pandemic have elevated funding and liquidity risks for Ideal. The company's financial flexibility in terms of unsecured debt / total debt remains low and its deposit base remains small and highly concentrated.

We expect Ideal's asset quality to be further weakened by the economic fallout from the pandemic. Its reported NPL ratio (greater than 180 days overdue) increased to 5.2% in FY20, from 3.2% in FY19, but was still below the average ratio for the sector.

Ideal's leverage in terms of debt/tangible equity has been supported by the capital infusions, but we expect it to increase in the medium-term as the company builds scale. Profitability, measured by pre-tax net income/average assets, dropped to 5.2% in FY20, from 6.0% in FY19, and is likely to remain under pressure due to rising credit costs.

Fintrex

Fintrex's rating reflects its weakened asset quality caused by its high risk appetite, which stems from its aggressive growth aspirations and evolving underwriting standards and risk controls. The rating also captures Fintrex's heavy reliance on secured funding and its small franchise.

We estimate that Fintrex's six-month NPL ratio exceeded 20.0% in FY20, almost triple the reported 7.7% in FY19, due to a sharp accumulation of NPLs caused by the weak operating environment and a contraction of the loan book. We see further downside risk to Fintrex's weaker-than-the-sector asset quality in FY21 due to the economic fallout from the pandemic. The company's loan loss allowance only covers around 50%-53% of its NPLs, below its historical coverage ratio of 68% during FY16-FY19, exposing its equity to provisioning risk.

Fintrex's predominant use of secured wholesale borrowings will hamper its financial flexibility in distressed market conditions. The share of unsecured debt in its funding mix continued to decline alongside a contracting deposit base. We estimate this ratio was around 17% in FY20 - one of the lowest among Fitch-rated finance and leasing companies - reflecting the low share of deposits in its funding mix. We do not expect a significant change in Fintrex's funding profile in the medium term.

We estimate that leverage, measured by debt/tangible assets, improved to around 2.8x in FY20, following a capital infusion of LKR430 million in 3QFY20. Nonetheless, the increased share of unprovided NPLs amid the company's small absolute equity size has exposed its capitalisation to credit shock.

We expect pressure on Fintrex's profitability, as measured by operating profit/average total assets, to extend into FY21 due to rising credit costs; we estimate that profitability plunged to around 1.0%-1.5% in FY20, from 4.0% in FY19, reflecting higher credit costs.

Bimputh

Bimputh's rating reflects its higher-than-peer leverage due to weak capitalisation and profitability, and increased pressure on funding conditions. The rating also captures its weakening asset quality, which we believe could intensify in the current challenging operating environment.

The Negative Outlook reflects the possibility for further downside risk caused by the economic fallout from the pandemic, which is likely to exacerbate the capital impairment by further pressuring Bimputh's already-weak profitability, causing heightened risk to its funding profile.

For Bimputh's key rating drivers, please see Fitch Downgrades Bimputh to 'B+(lka)'; Outlook Negative', at www.fitchratings.com/site/pr/10125356

RATING SENSITIVITIES

Factors that could, individually or collectively, lead to positive rating action/upgrade:

AMWCL

An improvement in AMW's ability to provide support would most likely result in an upgrade. However, the deterioration in AMW's credit profile in the current environment makes such an improvement unlikely in the near term.

Abans Finance

An upgrade of Abans' rating or a significant increase in Abans Finance's importance to its parent, which could be evident in a greater role in the group and/or a material increase in Abans' ownership that increases its propensity to provide support to the subsidiary. However, we do not expect such a change in the near term.

Ideal

We expect to resolve the RWP on completion of the phased increase in shareholding by MMFSL, when we have greater clarity on the linkages between Ideal and MMFSL and once we conclude our assessment of MMFSL's ability to provide support to Ideal. We will maintain the RWP beyond the typical six-month horizon, with parental support likely to be factored into the rating once MMFSL has acquired effective control of Ideal. Fitch's view of support will include an assessment the level of strategic importance of the Sri Lankan market and Ideal to MMFSL, the extent of integration and branding.

Fitch will remove the RWP if the investment is not completed. The rating would then remain driven by Ideal's intrinsic credit profile.

Fintrex

Positive rating action appears unlikely in the near term in light of the ongoing macroeconomic pressures. Sustainable improvement in asset quality measures, mainly through better underwriting standards and risk controls, while maintaining acceptable capitalisation commensurate with Fintrex's risk profile would be positive for its rating. Over the longer term, a substantial strengthening of the scale and franchise of the business would support positive rating actions.

Bimputh

Positive rating action appears unlikely in the near-term in light of the ongoing macroeconomic pressure and our expectation of further deterioration in the company's credit profile. In the longer term, an upgrade is contingent on a sustained improvement in Bimputh's credit metrics, especially its capital buffers, to be more commensurate with its risk appetite, stronger pre-impairment profit and better asset quality through an economic cycle.

The Outlook would be revised to Stable if we assess that the downside risks to Bimputh's credit profile have abated, especially where there is structural improvement in profitability and normalisation of asset quality, reducing pressure on its capital buffers.

Factors that could, individually or collectively, lead to negative rating action/downgrade:

AMWCL

A further weakening in AMW's credit standing, driven by its weakening performance, could lead to a reassessment of its ability to provide support to its subsidiary, and lead to a multiple notch downgrade on AMWCL. A decrease in AMW's propensity to provide support, likely due to a reduction in AMWCL's strategic importance or a significant dilution of AMW's shareholding, would also lead to a downgrade. The impact of any reduction in support on the national rating will be limited to two notches given the current assessment of the standalone strength of AMWCL.

Abans Finance

Any reduction in perceived support from Abans through, for instance, further dilution in the parent's shareholding to meet higher regulatory capital requirements or an increase in the scale of the business relative to the parent through organic or inorganic growth could be negative for its rating. The removal of parental support could result in a downgrade of the rating to the level of Abans Finance's Standalone Credit Profile, which could be multiple notches below its current rating.

A downgrade of Abans' National Long-Term Rating could also trigger a rating downgrade on Abans Finance.

Ideal

Ideal's rating is driven by its standalone profile. Negative rating action could occur if a severe deterioration in the operating environment, beyond our base-case expectations, were to diminish the company's asset quality, profitability and capital adequacy, leading to downward pressure on Ideal's standalone profile.

Fintrex

A significant reduction in loss absorption buffers owing to asset-quality slippage or further weakening in the funding and liquidity profile driven by the poor operating environment would pressure the rating.

Bimputh

Further capital impairment due to sustained losses and weak asset quality coverage, in the absence of a material capital infusion, may trigger a multiple notch downgrade. The inability to raise new capital to meet regulatory requirements could also lead to operational and funding-access constraints that would be negative for the rating.

Issuer Disclosure on Regulatory Action

A deposits cap of LKR2.05 billion has been placed by the Central Bank of Sri Lanka (CBSL) until Bimputh meets the required core capital as per Direction No. 02 of 2017 - Minimum Core Capital.

Abans Finance is in compliance with the minimum core capital set out in the Finance Business Act following CBSL's decision to defer the requirement of LKR2.0 billion until end-2020. As such, CBSL approved on 10 April 2020 for Abans Finance to freely canvas deposits up to LKR6.0 billion and upon reaching that limit may apply to CBSL to canvas additional deposits.

The "Issuer Disclosure on Regulatory Action" sub-heading was provided by the issuer and is included pursuant to applicable regulatory requirements. Fitch Ratings Lanka is not responsible for the contents of such information.

BEST/WORST CASE RATING SCENARIO

International scale credit ratings of Financial Institutions and Covered Bond issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of four notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from 'AAA' to 'D'. Best- and worst-case scenario credit ratings are based on historical performance. For more information about the methodology used to determine sector-specific best- and worst-case scenario credit ratings, visit [https://www.fitchratings.com/site/re/10111579]

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

PUBLIC RATINGS WITH CREDIT LINKAGE TO OTHER RATINGS

Abans Finance's rating is driven by those on its parent.

Video Story