August, 16, 2018

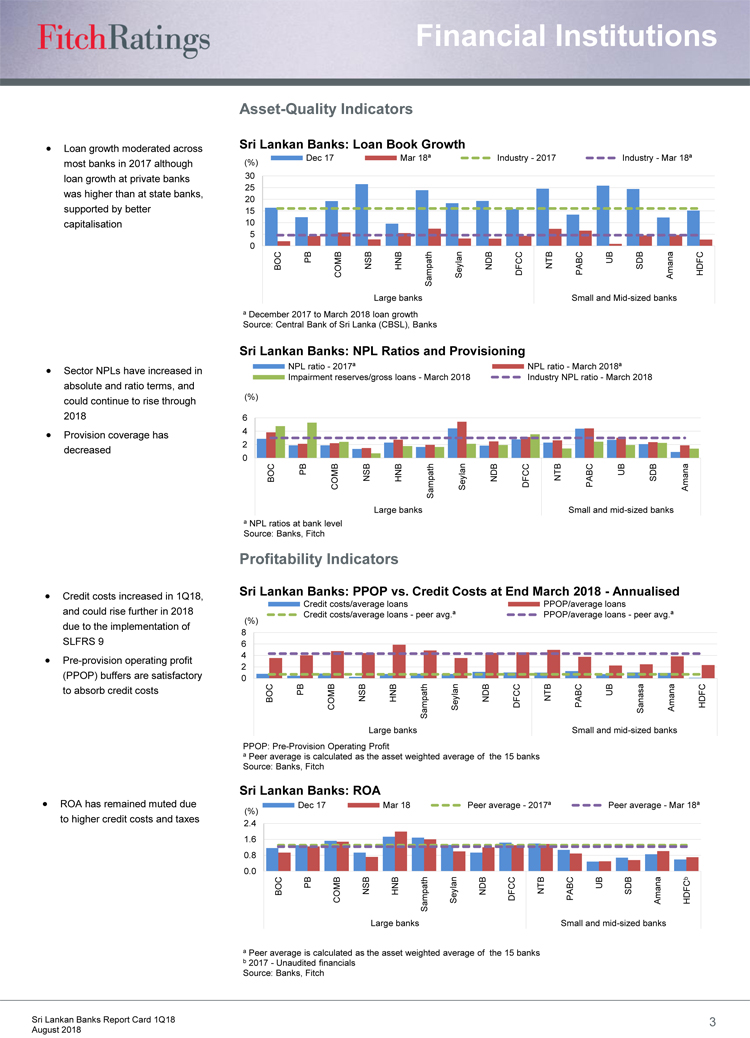

Fitch Ratings maintains a negative banking-sector outlook for Sri Lanka in 2018 as operating conditions should remain challenging, which could put mild pressure on performance during the rest of 2018 and possibly 2019. Nevertheless, the performance of Sri Lankan banks under Fitch's coverage remained fairly stable through 2017 and 1Q18, and Fitch expects their credit profiles to remain broadly intact.

The implementation of Basel III in 2017 prompted Sri Lankan banks to raise capital, leading to generally better capital ratios. Sri Lankan banks have raised Tier 1 capital of LKR66 billion and Tier 2 capital of LKR45 billion since 2017 ahead of the full implementation of Basel III in 2019. Further capital-raising is likely in 2018, although much of the shortfall was bridged in 2017.

Fitch does not expect a significant increase in NPL ratios despite risks to asset quality. The gross NPL ratio for the sector rose to 3.0% by 1Q18 from 2.5% at end-2017 due to a 25% increase in absolute NPLs on the back of difficult operating conditions. There has also been an increase in rescheduled loans in 2017 and in 1Q18 across Fitch-rated banks, indicating ongoing pressure on asset quality.

Higher credit costs could continue to hamper profitability in 2018. Credit costs rose in 1Q18, although pre-provision operating profitability buffers could still absorb the higher credit costs.

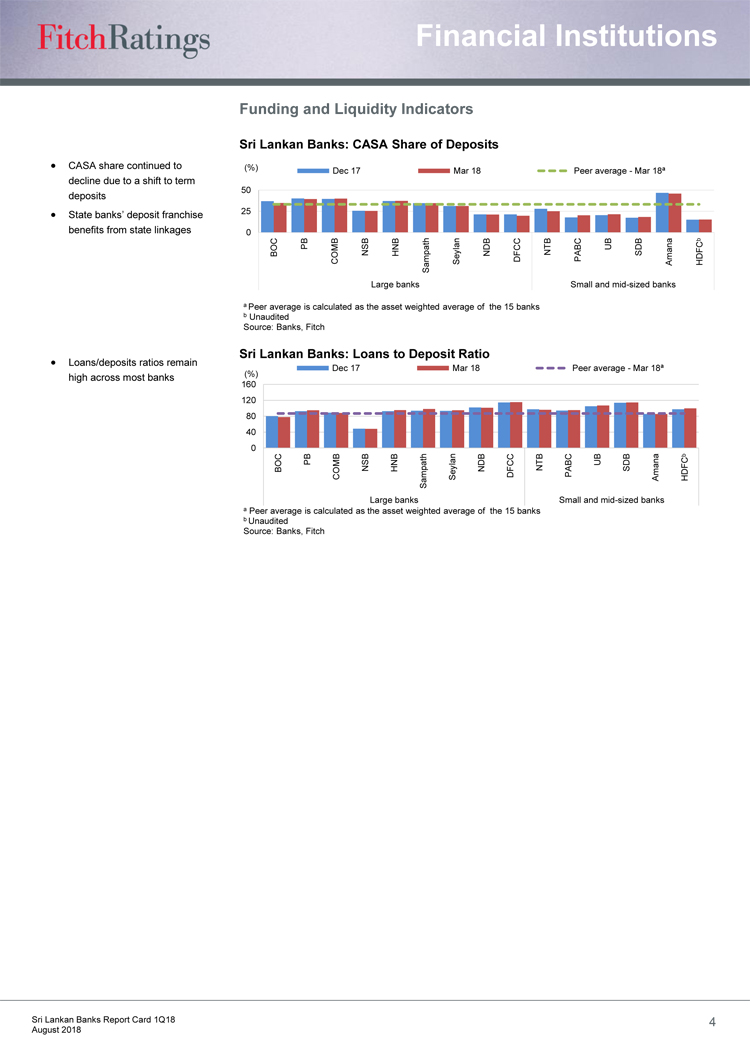

Fitch believes that deposits are likely to remain the main source of funding for Sri Lankan banks. The share of current and savings accounts for the sector had decreased due to the shift to term deposits on account of higher interest rates.

The implementation of SLFRS 9 in 2018 presents an additional challenge for Sri Lankan banks. The shift could add more pressure on capitalisation through a possible significant one-off adjustment, and drive a structural increase in normalised credit costs

Video Story