June, 1, 2020

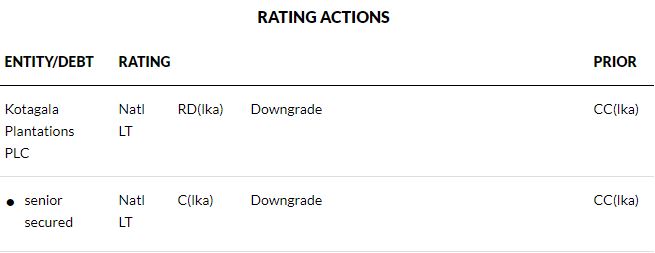

Fitch Ratings has downgraded Sri Lanka-based Kotagala Plantations PLC's (Kotagala) National Long-Term Rating to 'RD(lka)' (Restricted Default) from 'CC(lka)'. The National Rating on its outstanding senior secured debentures have been downgraded to 'C(lka)' from 'CC(lka)' to reflect low recovery prospects amidst significant prior ranking and secured debt.

KEY RATING DRIVERS

Missed Principal, No Grace Period: The downgrade reflects the company's confirmation that it did not pay the LKR250 million principal due on 26 May 2020 of its Type C secured redeemable debentures, and the absence of a grace period. The company says it will meet the aggregate interest payments of LKR34 million on the Type C and Type D debentures as scheduled, in line with the terms and conditions of the indenture.

Planned Debt Restructuring: Kotagala has announced that it intends to restructure the principal repayment on the Type C debentures, as well as the LK250 million principal due on its Type D secured redeemable debentures which are due on 26 May 2021. A completed debt restructuring would result in a rating upgrade to a level that reflects the company's post-restructuring capital structure and business risk. Conversely, Liquidation would result in a downgrade to 'D(lka)'.

Insufficient EBITDA Generation: Fitch does not expect Kotagala to be able to generate adequate EBITDA to cover its interest expenses and maintenance capex in the foreseeable future. This is in spite of profitable oil palm plantations contributing more to its EBITDA in the medium term, which will mitigate the losses in its structurally declining rubber business.

DERIVATION SUMMARY

The downgrade reflects payment default, and therefore Kotagala's rating is multiple-notches lower than the ratings of its closest peers on the Sri Lanka national scale.

KEY ASSUMPTIONS

- Revenue to decline by around 17% in FY20 and 12% in FY21 - owing to the disruption to the plantation industry stemming from the COVID-19 outbreak.

- EBITDA of around LKR100 million in FY20 and LKR70 million in FY21.

- Average capex of around LKR200 million per annum over FY20-FY21.

- No dividend payments during FY20-FY23.

RATING SENSITIVITIES

Factors that could, individually or collectively, lead to positive rating action/upgrade:

Following a possible financial restructuring and once sufficient information is available, the 'RD (lka)' rating will be upgraded to reflect the appropriate National Long-Term Rating for the post-restructuring capital structure, risk profile and prospects in accordance with our criteria.

Factors that could, individually or collectively, lead to negative rating action/downgrade:

Kotagala entering into bankruptcy filings, administration, liquidation or other formal winding-up procedures.

BEST/WORST CASE RATING SCENARIO

International scale credit ratings of Non-Financial Corporate issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of four notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from 'AAA' to 'D'. Best- and worst-case scenario credit ratings are based on historical performance. For more information about the methodology used to determine sector-specific best- and worst-case scenario credit ratings, visit https://www.fitchratings.com/site/re/10111579.

LIQUIDITY AND DEBT STRUCTURE

Poor Liquidity: As of the nine months ended December 2019, Kotagala had only LKR55 million in cash to meet LKR1 billion in secured debt maturities - excluding debenture principal - falling due within the following 12 months. Kotagala does not have the necessary funds to meet near-term debt obligations, and access to new capital is poor. Kotagala also has no unutilised credit lines to help ease its liquidity position. The company also has outstanding statutory payments amounting to around LKR900 million - which we expect to be delayed further until the company is able to reorganise. Apart from meeting principal payments, Kotagala's ability to service its interest obligations remains a challenge in itself, as we expect EBITDA/interest paid to remain below 1.0x (last 12 months ended December FY20: -1.3x).

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

Video Story