April, 28, 2026

The Financial Times - Oil hit $110 for the first time in three weeks on Tuesday as the US and Iran appeared to make little progress towards a peace deal that would unlock energy supplies through the Strait of Hormuz.

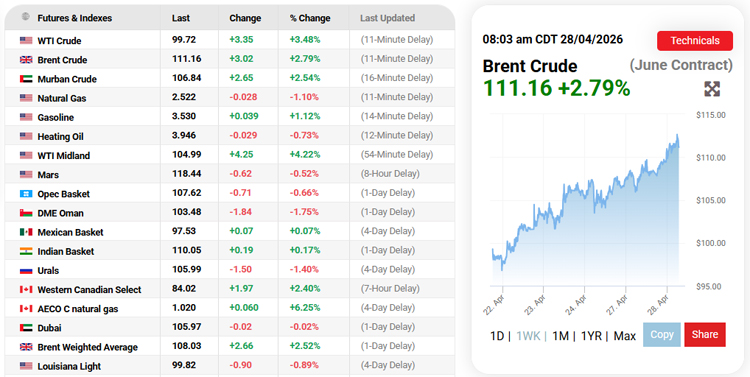

Brent crude, the international oil benchmark, rose as much as 4.1 per cent to highs of $112.70 a barrel on Tuesday, putting pressure on government bond markets as investor worries over inflation grew.

The White House said on Monday that US officials were discussing Iran’s latest proposal, which has not been made public, but maintained “red lines” on any deal to end the eight-week war, including preventing Tehran from obtaining a nuclear weapon.

White House press secretary Karoline Leavitt told reporters that President Donald Trump had convened national security officials to review the proposal. “His red lines with respect to Iran have been made very, very clear,” she said, adding that Trump would address the matter “very soon”.

Speaking on Monday, US secretary of state Marco Rubio said there were “questions” over Iran’s offer and said Tehran’s nuclear programme remained a “fundamental issue [that] still has to be confronted”.

“It’s better than what we thought they were going to submit. I think there are still questions about whether the person submitting it had the authority to submit that offer,” Rubio told Fox News.

Asked whether the US would accept an offer by Iran to open the strait while delaying talks over Tehran’s nuclear programme, Rubio said he would not speculate on what Trump might do.

“Suffice it to say that the nuclear question is the reason why we’re in this in the first place . . . that still remains the core issue,” he said.

Brent crude soared from less than $60 a barrel at the start of the year to as high as $119 at its peak during the conflict as Iran brought traffic through the Strait of Hormuz to a near halt and attacked energy facilities across the Gulf.

West Texas Intermediate, the US benchmark, gained 4 per cent by morning trading in New York to trade around $100.17 a barrel.

“Markets have been latching on to any signs of peace talks, and the absence of that is raising fears that they are not going to happen,” said Jim Reid, head of macro research at Deutsche Bank.

This move higher in oil has also reignited bets that central banks will have to lift interest rates to contain the resulting wave of inflation, hitting bonds in the US, Europe and the UK. In the UK, where government debt has proven particularly vulnerable to the energy shock, the 10-year gilt yield rose 0.05 percentage points in early trading to break above 5 per cent for the first time since late March. Bond yields rise as prices fall.

The latest sell-off has also pushed longer-dated 30-year yields to 5.7 per cent, within touching distance of their highest level this century.

“The longer the Strait is closed, the more it would have a negative impact on the global economy,” said Mohit Kumar, chief European economist at Jefferies.

Video Story