October, 8, 2019

Previous Pre-Policy report; CBSL reduces its policy rates by 50 bps

Contrary to our expectation, CBSL, decided to reduce SDFR and SLFR by 50bps each to 7.00% and 8.00% respectively, one policy meeting ahead of our forecast, with the aim of boosting credit flows to productive sectors and in turn to assist the revival of the economy.

CBSL undertook a number of measures to improve the growth of the economy

GDP growth for the 2Q2019 recorded at 1.6% significantly lower compared to 3.9% recorded in 2Q2018. In order to address the overly sluggish credit growth, over the past 11 months, CBSL undertook a number of monetary policy and regulatory measures to induce a reduction in market lending rates and thereby boost the GDP growth of the country. Accordingly, CBSL reduced its policy rates by 50bps each in May and Aug and also reduced the SRR applicable on rupee deposit liabilities of Licensed Commercial Banks by 2.50% in order to improve the liquidity in the financial market. These measures were expected to stimulate the demand for credit while improving GDP growth of the country.

Imposition of lending caps to further enhance the credit flows

The growth of credit extended to the private sector has increased marginally by 1.16% since the beginning of this year, remaining far below the levels observed in the corresponding period of 2018, while NPLs have grown due to various factors. CBSL is of the view that, excessively high nominal and real lending rates are a key reason for slowing credit expansion and rising NPAs. Moreover, SL's real lending rates are found to be unacceptably high compared to its peer economies. Accordingly, the Monetary Board decided to order the Licensed Banks to reduce interest rates applicable on all rupee denominated loans and advances by at least 200bps by 15th Oct 2019, in comparison to the interest rates applicable as at 30th Apr 2019. Moreover, in the case of credit card advances, the maximum interest rate applicable has been reduced to 28% per annum. These measure are expected to lower market lending rates by banks, thereby boosting credit flows to productive sectors. This, along with improved repayment capacity of borrowers at lower interest rates, was expected to strengthen licensed banks, by addressing the challenge of rising NPLs.

Raising USD500.0Mn via Samurai Bonds to add more cushion to foreign reserves

The Government appointed a bid manager to raise USD500.0Mn via Samurai bonds while the issuance will take place in Oct or Nov ahead of the presidential election. We expect at present foreign reserves (USD 8.5Bn as at 30th Aug) are at a comfortable stage with sufficient foreign repayment cover suggesting the lower foreign currency requirement. The new Samurai Bond issue is expected to add a further cushion to foreign reserves.

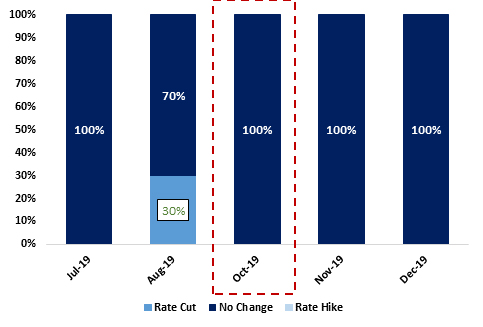

Sri Lanka to hold its election in November while creating an uncertainty during that period

CBSL is extremely unlikely to change its key monetary policy rates amidst the uncertainty hovering with the presidential election around the corner. The reduction of policy rates in Aug which was way in advance also supported this view.

Rupee depreciated slightly by 1% amidst foreign outflows amounting to LKR 13.8Bn since the previous rate cut

Since the previous rate cut in Aug 23rd, Rupee depreciated by 1% amidst the foreign outflows amounted to LKR 13.8Bn which resulted in foreign holdings in Government Securities declining below 2%, lowest in recent times

Expectation

Considering the previous 50bps rate cuts each in May and Aug and imposition of lending caps, First Capital Research believes that policy change is not required for the year 2019 while allowing the impact of previous policy decisions to materialise. Accordingly, we expect Monetary Board to hold rates for the rest of the year 2019.

Video Story