November, 15, 2023

The targets laid out in Sri Lanka’s budget for 2024 will be challenging to meet, even with the economic recovery that we expect to continue next year, says Fitch Ratings. The fiscal deficit is set to be wider than our current forecast of 7.1% of GDP in 2024 in light of the new data, even after excluding bank recapitalisation costs, and the revenue/GDP ratio will be lower than we had assumed.

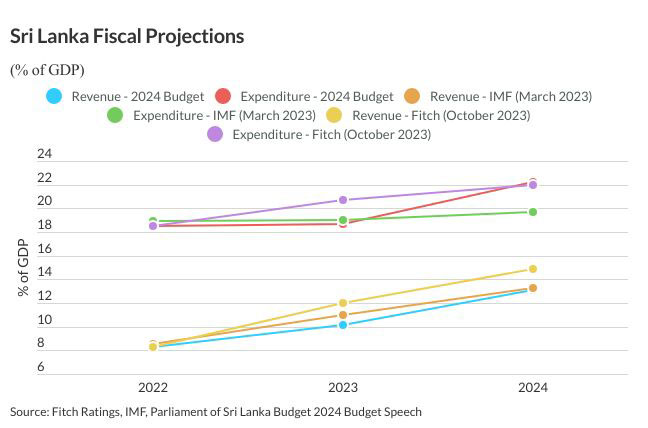

The government is targeting a budget deficit of 9.1% of GDP in 2024, wider than a revised estimate of 8.5% in 2023. However, without bank recapitalisation costs, the deficit in 2024 would be a narrower 7.6% of GDP. Excluding recapitalisation costs, the budget targets a primary surplus of 0.8% of GDP in 2024, against a deficit of 0.7% in 2023. However, including recapitalisation costs pushes the 2024 primary deficit target to 0.6% of GDP.

The primary surplus goal for 2024, excluding bank recapitalisation, is broadly in line with the 0.8% of GDP projected by the IMF in March when it approved Sri Lanka’s USD3 billion Extended Fund Facility (EFF). We also see the revenue target as relatively aligned. However, the government’s expenditure target for 2024, at 22.2% of GDP, is somewhat higher than the 19.7% the IMF had envisioned and well above the revised budget estimate of 18.7% for 2023.

The release of the next tranche of EFF financing, worth around USD330 million, will depend partly on the IMF’s assessment of Sri Lanka’s progress in securing financing assurances from official creditors. Fitch believes there has been some progress since March, but the timeline for a restructuring deal with official creditors remains unclear.

Fitch believes there are significant risks to the government’s revenue goal for 2024. Sri Lanka has a record of fiscal slippage, and revenue collection fell 29% short of target over 9M23. The authorities aim to raise revenue by almost 45% in 2024. This will be aided by a planned 3pp increase in the value-added tax to 18%, but the boost to revenue from inflation is set to weaken in 2024. We project consumer prices will rise by 8.7% on average in 2024, compared with 22.1% in 2023. The lift from economic growth, which Fitch projects at 3.3% in 2024, will also be modest.

Downside risks to revenue could be offset by lower-than-budgeted spending. We think the presidential election in late 2024 will incentivise the government to keep to its spending plans, which include a 14% increase in spending on salaries and wages. Nevertheless, if revenue falls short, there may be some room to trim capital expenditure, which amounts to almost 20% of total planned spending and is budgeted to rise 55% in 2024, excluding bank recapitalisation.

The government’s efforts to implement governance reform after a recent diagnostic study by the IMF may also support revenue collection. The budget proposes to establish a new revenue authority under the Ministry of Finance to improve tax collection, and a new investment law will look to establish a National Economic Commission to promote investment. However, it will take time to assess these bodies’ effectiveness.

Fitch rates Sri Lanka’s Long-Term Foreign-Currency Issuer Default Rating (IDR) at 'RD' (Restricted Default). We may move the IDR out of ‘RD’ upon the sovereign’s completion of a commercial debt restructuring that we judge to have normalised the relationship with the international financial community. Sri Lanka’s post-default rating would depend upon our assessment of its credit profile. Fitch upgraded Sri Lanka's Long-Term Local-Currency IDR to 'CCC-' in September, reflecting the completion of the local-currency portion of Sri Lanka's domestic debt optimisation plan.

Video Story