April, 28, 2020

The effects of COVID-19 on banks in Asia-Pacific (APAC) will be more severe than those of a normal cyclical downturn, says Fitch Ratings in its latest report.

Operating environments in the region will be significantly affected over the next two years, with weaker domestic and international economies reducing growth prospects and increasing the risk of asset-quality deterioration.

"We expect these trends to erode banks' loss-absorption buffers, raising their sensitivity to financial stress," the rating agency said.

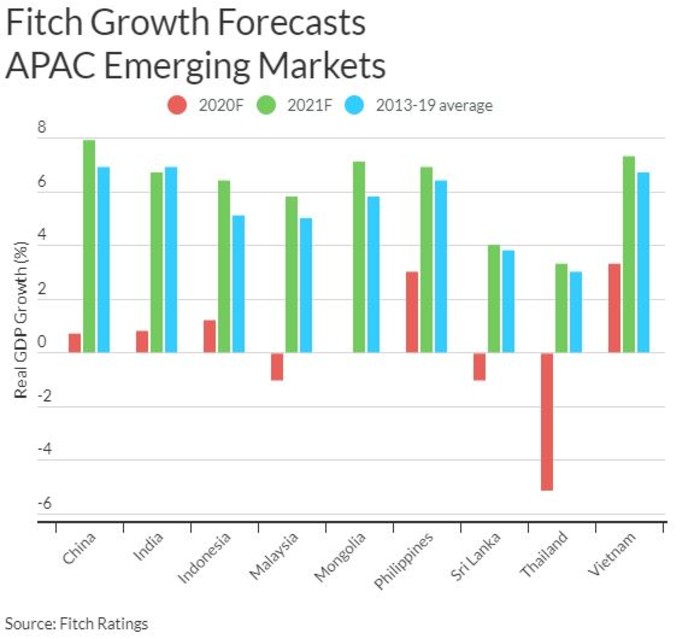

"Our latest forecasts project a sharp slowdown in global economic growth in 2020. Within Asia, China and India will post their slowest expansion in decades, and growth in many other markets will hit multi-year lows. We expect a recovery in 2021, although most economies will still lag longer-term growth averages and some will not recoup the contraction expected in 2020," it added.

Fitch adopts a 'through-the-cycle' approach in our rating assessments. However, the pandemic is not comparable with a regular cyclical downturn. The downside shock has been faster and deeper than in a normal cycle, and the damage associated with job losses and business closures may linger despite higher 2021 GDP growth in many markets.

"We expect adverse effects on bank profitability will be more enduring than in a normal cycle. In some cases, deterioration in asset quality may not become apparent until next year, when the effect of government policy measures introduced to offset the crisis begins to fade. Reflecting this, we have adjusted our annual sector outlook for bank performances to negative for all 17 banking systems in APAC," Fitch said.

"Against this background, we see more banks hitting downside rating triggers - particularly those whose ratings are already on negative outlook - with stressed financial metrics or weaker operating environments being sustained across and beyond our two-year outlook period. As such, more banks will be downgraded if they hit (or are likely to hit) rating triggers such as structurally lower profitability or weaker capital. This will apply particularly if there is evidence of deterioration in asset quality exceeding our expectations under baseline scenarios."

"Banks with the lowest loss-absorption buffers or headroom at any given rating level will face the greatest risk of negative rating action, particularly if our macro and bank-specific financial metrics forecasts shift closer to the current downside scenarios. We will also take into consideration evidence of financial profile deterioration in prior stress situations and vulnerability to stress, notably assessing whether we view risk appetite to have increased relative to risk buffers in recent years."

"The deeper the shock and the shallower the recovery, the longer it will take for banks' credit profiles to be commensurate with higher ratings. On the other hand, if we assess any deterioration as likely to be moderate, or expect banks to recover within the next two years, then ratings action may be limited to negative outlooks. Our analysis will also reflect the extent or nature of any measures taken by policymakers, and how these may affect banks over the longer term," it added.

Around half of bank Issuer Default Ratings (IDRs) in APAC are driven by expectations of external support, mainly from sovereigns. Among emerging markets, external support underpins two-thirds of bank IDRs. In such cases, an individual bank's IDR may be unaffected even if we downgrade our assessment of its standalone Viability Rating. Nonetheless, the impact of the coronavirus and governments' policy responses could also affect the ratings of supporting entities, including sovereigns, and in these cases bank rating actions could mirror those of their supporting entity.

Video Story