October, 7, 2020

Moody’s Investors Service says in a new report that despite substantial risks, Asia-Pacific banks’ creditworthiness should remain largely intact through the current economic downturn.

“We expect asset quality to deteriorate significantly as economic conditions remain weak, while profitability will take a hit from rising credit costs and declining margins,” says Eugene Tarzimanov, a Moody’s Vice President and Senior Credit Officer.

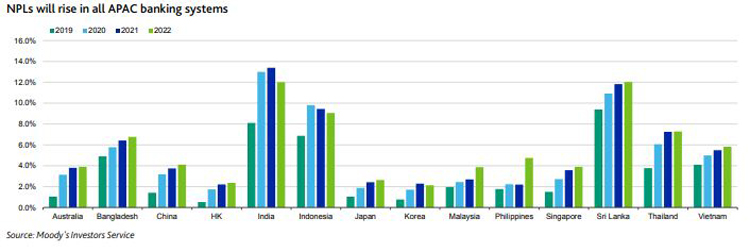

Moody’s expects problem loans will double on average across the 14 APAC economies by 2022, with banks in India and Thailand to see the largest increases due to the severity of the economic shocks and the historically poor performance of certain loan types.

Meanwhile, rising credit costs and a 5%-10% drop in pre-provision income amid falling interest rates will drive a significant deterioration in profitability in coming years.

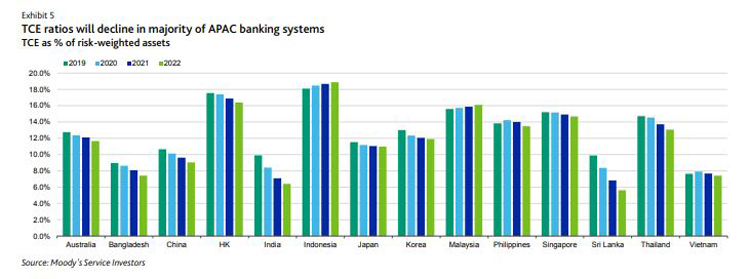

“In line with weak operating conditions, we expect capital ratios will decline at 78% of the 218 rated APAC banks by the end of 2022 from the end of 2019,” adds Tarzimanov.

“However, the decline at most rated banks will not be significant enough to prompt a change in our views on fundamental creditworthiness, which also take into account other factors such as profitability, asset quality, funding and liquidity.”

Further, Moody’s estimates that core capital, as measured by TCE as a percentage of RWAs, will decline at 78% of 218 banks in APAC by the end of 2022 from the end of 2019.

"TCE ratios will fall by up to 100 basis points at 31% of banks in the sample and by 100 basis points-200 basis points at 25%. A further 22% will see drops of more than 200 basis points, moderately higher than 18% in Europe, US, UK, Mexico and Brazil," it said.

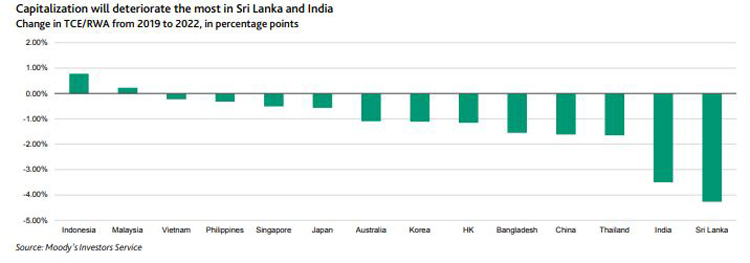

"Among the 14 APAC banking systems, TCE ratios will decline the most significantly in Sri Lanka and India due to the severity of economic shocks to the countries, banks’ weaker starting solvency metrics, and historically weak underwriting. By contrast, capitalization will strengthen in Indonesia as a result of banks' strong profitability," it added.

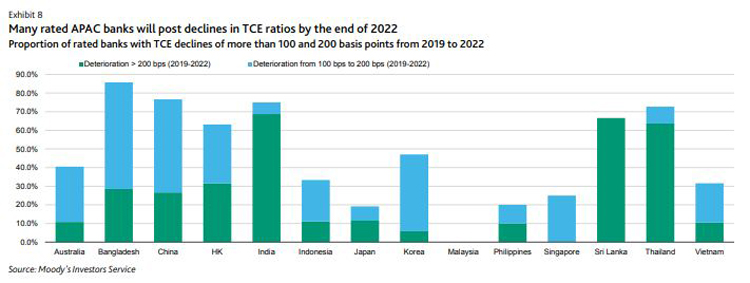

Moody’s further noted that Changes in capital ratios will vary significantly among individual banks.

"TCE ratios at the majority of rated banks in India, Thailand and Sri Lanka will plunge by more than 200 basis points by 2022, while in other economies, the proportion of such weak performers will range from 10% to 30% of rated banks. In Malaysia, no bank will lose more than 100 basis points of TCE."

"While the drop in Chinese banks’ TCE ratio is 162 basis points between 2019 and 2022, the scenario has not considered the highest NPL provision coverage among all APAC banking systems. At the end of 2019, NPL coverage for the Chinese banking system reached 186%, while that for the rated banks was at 221%. We expect that authorities will allow a lower NPL coverage for banks in case of a significant increase in NPLs, therefore reducing the hit to TCE ratios of Chinese banks," it said.

Additionally, the economic performance of China post coronavirus outbreak has been better than expected and Moody’s has improved its forecasts for China’s GDP.

"Given this recent upward revision in GDP, we expect a lower impact to TCE ratios for Chinese banks. As a whole, our model shows that about 80% of rated APAC banks will be adequately positioned at their current ratings, despite falls in capital. The other 20% are banks that will suffer TCE erosion of more than 200 basis points. While the risk of creditworthiness deterioration is greater for these banks, some of them are likely to take steps to strengthen their solvency, such as raising new capital." it said.

Moody's further stated that government measures to support borrowers will provide modest capital relief for banks.

"In APAC economies, government guarantees and other support schemes will curb buildups in NPLs. Governments have implemented various support measures to lessen the economic impact of the pandemic. While our GDP forecasts incorporate the benefits of fiscal support measures, which trickle down to our model for banks, our NPL projections do not factor in the effects of schemes to support borrowers, such as debt moratoriums, the provision of loans at subsidized rates and guarantees."

"Among other measures, government guarantees for SME loans are an integral part of efforts to protect jobs and ultimately public consumption. However, they will provide a limited boost to capital for banks in APAC, as seen in the cases of Korea and Thailand, where banks have large SME exposures."

"In Korea, credit guarantees cover 70%-100% of default risks from SME and sole proprietorship (SOHO) loans for small businesses and retailers, equaling a maximum of 4% of total outstanding SME and SOHO loans. They will boost banks’ TCE ratios only by about 7 basis points by 2022 by reducing loss given defaults. In Thailand, guarantees for SME loans cover around 30% of default risks, with the maximum guarantee size at about 5% of total SME loans in the system, so they will give a marginal boost to TCE," it said.

Video Story